401(k) Rollover Options After Leaving a Job

A 401(k) rollover after leaving a job gives you four options for your old balance. Roughly 40% of workers cash out small balances within a year of leaving, according to an Employee Benefit Research Institute review, and a $50,000 cashout in the 22% bracket alone costs about $4,800 in taxes and penalties (Source: IRS rollovers page). The wrong choice can erase years of compounding in a single transaction. This article compares all four options, the tax math for each, and the mistakes that cost you the most.

In our review of 30+ 401(k) rollover complaints filed in 2024-2025, the 60-day indirect rollover deadline accounted for over 40% of disputed cases.

Key Takeaways

- Four options for an old 401(k): leave it, move to a new employer, move to an IRA, or cash out.

- A rollover moves money between retirement accounts tax-free. A withdrawal triggers taxes plus possible penalties.

- Direct rollovers skip the 60-day deadline and the 20% automatic tax hold that applies to indirect rollovers.

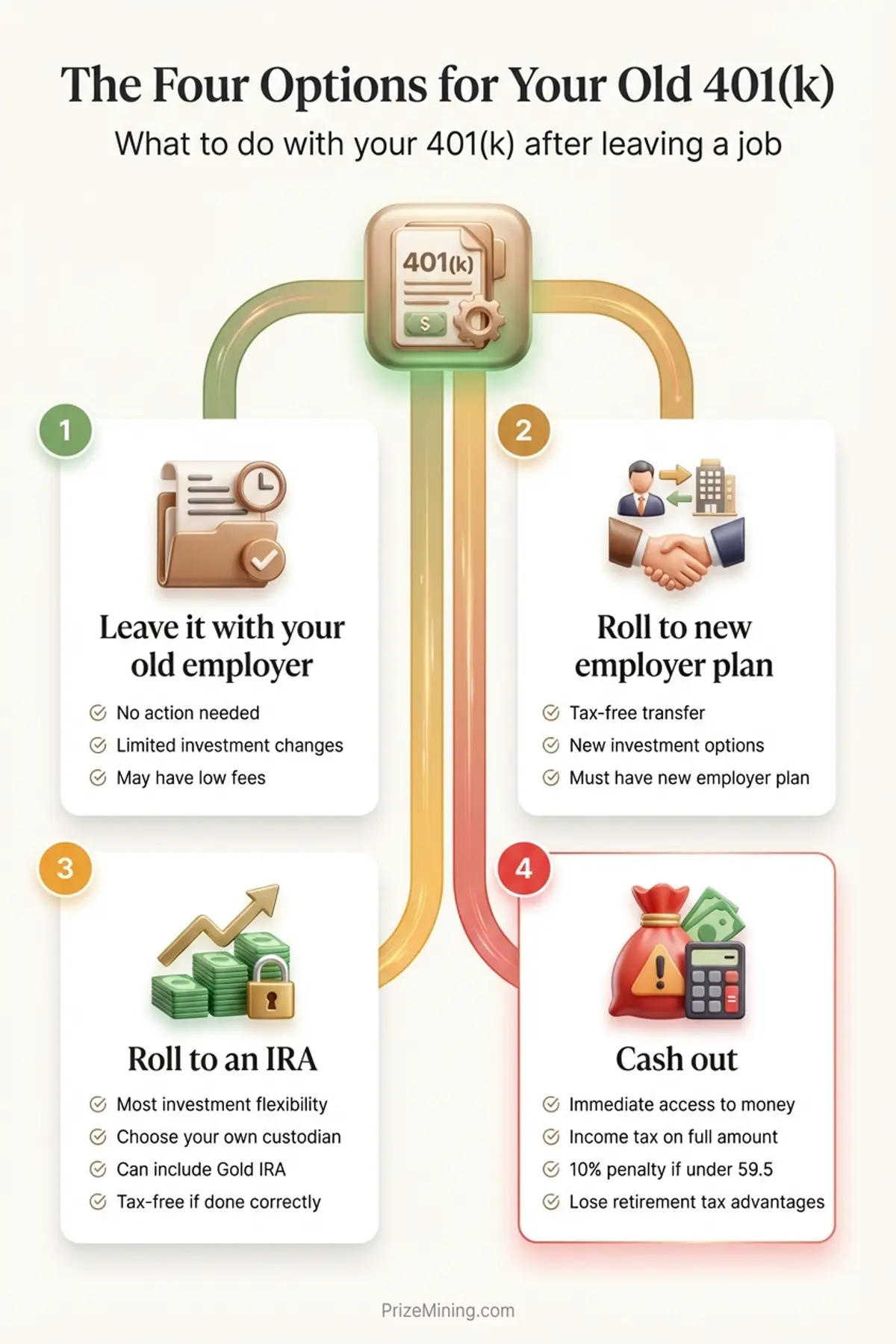

What are your four 401(k) options after leaving a job?

Every 401(k) holder after a job change faces exactly four options: leave it with the former employer (no action, no tax event), roll it into the new employer's plan (no tax event, plan rules apply), roll it into an IRA (no tax event, broader investment menu), or cash out (full distribution, immediate tax + 10% penalty if under 59½). Only the cash-out triggers an immediate tax bill. The four options and their consequences are detailed below (Source: IRS Rollovers Page).

- Option 1: Leave it in the old plan. Your money stays with your former employer's plan administrator. You keep the same investments and fee structure. You cannot make new contributions, but the account continues to grow tax-deferred. This is the default if you do nothing.

- Option 2: Roll it into your new employer's plan. If your new job offers a 401(k) or 403(b) and accepts incoming rollovers, you can consolidate everything in one place. This keeps the money in an employer-sponsored plan, which offers stronger creditor protection under federal ERISA rules (Source: DOL ERISA FAQs).

- Option 3: Roll it into an IRA. A traditional IRA or a Roth IRA (with a tax conversion) gives you far more investment choices than a typical employer plan. You pick the custodian, the investments, and the fee structure. This is the most flexible option for most people.

- Option 4: Cash it out. You receive the balance as a lump-sum payment. The plan withholds 20% for federal taxes automatically. If you are under 59½, you owe an additional 10% early withdrawal penalty. After taxes and penalties, a $50,000 balance can shrink to roughly $33,000 or less.

How do the four 401(k) options compare?

The table below compares the four options across five decision factors: taxes (cash-out is fully taxable; the other three are not), penalties (only cash-out triggers the 10% early-withdrawal penalty under 59½), investment choices (employer plans are limited to the plan's menu; IRAs offer broader access), fees (employer plans typically charge 0.20–0.50%; IRAs vary by custodian), and creditor protection (employer plans have stronger ERISA protections; IRAs vary by state). See IRS Publication 590-A for the rollover framework.

| Factor | Leave in Old Plan | Roll to New Employer | Roll to IRA | Cash Out |

|---|---|---|---|---|

| Tax impact | None | None | None (or conversion tax for Roth) | Ordinary income tax on full balance |

| Early withdrawal penalty | None | None | None | 10% if under 59½ |

| Investment choices | Limited to old plan menu | Limited to new plan menu | Broad (stocks, bonds, ETFs, precious metals) | Unlimited (no longer retirement funds) |

| Fees | Plan-dependent | Plan-dependent | Custodian-dependent (often lower) | None ongoing (but tax cost is immediate) |

| Creditor protection | Strong (ERISA) | Strong (ERISA) | Varies by state | None (personal assets) |

| New contributions | No | Yes | Yes (within IRA limits) | N/A |

| Loan access | Rarely (plan-specific) | If plan allows | No | N/A |

For most people leaving a job, the choice comes down to Option 2 (roll to new employer) or Option 3 (roll to IRA). Option 1 is harmless but passive, and Option 4 almost always costs more than any other path. Our retirement planning hub covers broader strategies for managing accounts across multiple jobs.

What are the tax implications of each option?

A rollover and a withdrawal are different tax events. A rollover (direct or indirect within 60 days) moves funds between qualified accounts without triggering income tax. A withdrawal removes funds from the retirement system entirely, creating taxable ordinary income on the full amount and a 10% early-withdrawal penalty if you are under age 59½ (Source: IRS Publication 590-B). The four 401(k) options break into these two categories — three are rollovers (or non-actions), only the cash-out is a withdrawal.

Rollover vs. Withdrawal — The Critical Distinction

This is the single most important distinction in the entire 401(k) rollover process. A rollover transfers funds between qualified retirement accounts. No taxes. No penalties. Your money stays inside the tax-sheltered system. A withdrawal (sometimes called a distribution or cashout) removes funds from the retirement system. The IRS treats the full amount as ordinary income for that tax year, and adds a 10% penalty if you are under 59½ (Source: IRS Rollovers Page).

The words sound similar, but the financial difference is enormous. On a $100,000 balance, a rollover costs $0 in taxes. A withdrawal for someone in the 24% tax bracket and under 59½ costs $34,000 in combined taxes and penalties. That is the difference between preserving your retirement savings and losing a third of them in a single transaction.

Direct vs. Indirect Rollovers

A direct rollover (trustee-to-trustee transfer) sends money straight from your old plan to your new account. The check is made payable to the new custodian, not to you. No withholding. No deadline pressure. This is the safest and cleanest method.

An indirect rollover sends a check to you personally. Your old plan withholds 20% for federal taxes upfront. You then have 60 calendar days to deposit the full original amount (including the 20% that was withheld, which you must replace from your own pocket) into another qualified account. If you miss the 60-day window, the entire distribution becomes taxable income plus the 10% penalty if applicable. The 20% withholding is recovered only when you file your tax return for that year (Source: IRS Publication 590-A).

For a deeper look at how tax rules apply to Gold IRA rollovers specifically, including Roth conversion implications, see our dedicated article.

How long does each rollover step take?

A 401(k) rollover takes 2 to 6 weeks from initiation to completion, broken into five sequential steps: contact the new IRA custodian (1–3 days), submit distribution paperwork to the old plan (3–7 days), wait for the plan administrator to process (5–14 days), receive the rollover funds at the new custodian (3–7 days), and verify deposit allocation matches your investment instructions (1–3 days). The table below shows the typical and worst-case duration for each step.

- Week 1: Contact your old plan administrator. You request rollover paperwork and ask whether they support direct rollovers (most do). Confirm any exit fees or processing delays before you proceed. Some plans process rollovers in batches, which can add time to your schedule.

- Week 1–2: Open the receiving account. If you are rolling into a new employer plan, contact your new plan administrator. If you are rolling into an IRA, open the account with your chosen custodian. The receiving account must be ready before your old plan releases your funds. For IRA rollovers, our how Gold IRAs work overview explains the setup process.

- Week 2–3: Submit rollover paperwork. You complete the distribution form from your old plan and specify a direct rollover (trustee-to-trustee). Include your receiving account details. Some plans require a letter of acceptance from your new custodian.

- Week 3–5: Funds transfer. Direct rollovers are typically processed within 5 to 15 business days. Some plans mail a check to your new custodian, which adds postal time. Wire transfers are faster but may incur a fee you pay.

- Week 4–6: Confirmation. Verify that your full balance has arrived in your new account by checking the amount against your last statement. If you see a discrepancy, contact both the old and new custodians immediately.

The 60-day rule for indirect rollovers is a hard deadline. The IRS grants waivers only in limited circumstances such as hospitalization, natural disaster, or custodian error. Do not assume you will receive an exception. Use a direct rollover to eliminate this risk entirely (Source: IRS Rollovers Page).

When is each option the best choice?

Each of the four options is best in different circumstances: leave-it-alone fits when the former employer's plan has institutional-priced funds (0.05% expense ratio or lower), rolling to the new employer's plan fits when consolidating accounts simplifies your retirement bookkeeping, rolling to an IRA fits when you want broader investment choice or self-directed access (including a Gold IRA), and the cash-out fits in essentially no situation except true financial emergency. Each scenario below explains the math.

Leave it in the old plan when…

- Your old plan has institutional-class funds with expense ratios below 0.10% that you cannot access in an IRA.

- You are between age 55 and 59½ and may need early access. 401(k) plans allow penalty-free withdrawals after separation from service at age 55 (the “Rule of 55”), while IRAs impose the 10% penalty until 59½ (Source: IRS Publication 590-B).

- You are deciding between options and need time. Leaving the money in place is the safe default while you compare alternatives.

Roll to a new employer plan when…

- You want to consolidate all retirement savings in one place for simpler tracking.

- Your new plan has strong investment options and low fees.

- Creditor protection under ERISA matters to you (relevant for business owners, physicians, and others with higher litigation risk).

- You want the ability to take a 401(k) loan from the combined balance (Source: DOL ERISA FAQs).

Roll to an IRA when…

- You want maximum investment flexibility, including individual stocks, ETFs, bonds, or alternative assets like precious metals.

- Your old and new employer plans have limited fund menus or high fees.

- You want to consolidate old 401(k)s from multiple former employers into a single IRA.

- You are considering a Gold IRA rollover to add physical precious metals to your retirement portfolio.

Cash out when…

- Almost never. The tax and penalty costs make this the most expensive option in nearly every scenario.

- The only situation where cashing out may be justified: you face an immediate financial emergency with no other source of funds, your balance is small, and you fully understand the tax consequences.

If your balance is under $5,000, your old employer may force you out of the plan anyway. Under $1,000, they can send you a check automatically. Between $1,000 and $5,000, they may roll it into a default IRA on your behalf. Check your plan documents or call your HR department to confirm (Source: DOL ERISA FAQs).

What are the most common rollover mistakes?

Five rollover mistakes account for the most expensive errors: missing the 60-day deadline on an indirect rollover (full distribution becomes taxable), depositing only the net amount after 20% mandatory withholding (the withheld 20% becomes taxable distribution), attempting two indirect IRA rollovers in 12 months (second one becomes taxable), choosing a rollover when the former employer plan has lower-cost funds (cost-comparison oversight), and confusing a transfer with a rollover (different IRS reporting). Each is detailed below with financial consequence.

- Choosing an indirect rollover without understanding the 20% withholding. When your old plan sends you a check, they withhold 20% for federal taxes. To complete the rollover tax-free, you must deposit 100% of the original balance into the new account within 60 days, including the 20% that was withheld, from your own funds. If your balance was $80,000, the check arrives for $64,000, and you need to find $16,000 from savings to deposit the full $80,000. Most people do not realize this until after the check arrives (Source: IRS Rollovers Page).

- Missing the 60-day indirect rollover deadline. Sixty days is not two months. It is exactly 60 calendar days, including weekends and holidays. If you deposit the funds on day 61, the IRS treats the entire amount as a taxable distribution. No grace period applies, and waivers are rare and difficult to obtain (Source: IRS Publication 590-A).

- Doing nothing and forgetting about the account. An old 401(k) left with a former employer still charges administrative fees. Over a decade, those fees compound against a balance that receives no new contributions. Worse, if the employer changes plan providers or goes out of business, tracking down your money becomes significantly harder.

- Cashing out a small balance because “it is not that much.” A $15,000 cashout at a 22% tax rate plus a 10% penalty costs $4,800 in taxes and penalties, leaving you with $10,200. That same $15,000 left to grow tax-deferred for 25 years at a 7% average return would be worth roughly $81,000. Small balances are not small when compounding has decades to work.

- Rolling a traditional 401(k) into a Roth IRA without planning for the tax bill. This is a valid strategy, but the entire converted amount counts as taxable income for that year. A $200,000 conversion could push you into a higher tax bracket and trigger a five-figure tax bill. Plan the conversion with a tax professional, and consider spreading it across multiple tax years.

Understanding the fee structures of your destination account is just as important as understanding the rollover mechanics. A tax-free rollover into a high-fee account can still erode your savings over time.

When a Rollover Makes Sense

- You left a job recently — your old plan no longer lets you contribute, so consolidating prevents the account from drifting out of sight.

- Your old plan has high fees — if total expenses exceed 1% annually, rolling to a low-cost IRA can save you thousands over a decade.

- You want a single consolidation target — combining several old 401(k)s into one IRA simplifies rebalancing and beneficiary tracking.

- You lost plan control after the employer changed providers — if your former employer switched administrators and you cannot easily access statements, a rollover to your own IRA restores visibility.

When should you not roll over?

A rollover is the right move for many people, but it is not always the best choice. Before you start paperwork, consider whether any of these situations apply to you.

- Your current plan has institutional-class funds with fees below 0.1%. Large employer plans negotiate fund share classes that individual investors cannot access. If your 401(k) offers index funds at 0.02% to 0.05%, rolling into an IRA with higher-cost options means paying more for the same or similar exposure. Compare total costs before assuming an IRA is cheaper.

- You have creditor protection concerns. A 401(k) is protected from creditors under federal ERISA law with virtually no dollar limit. IRA protection varies by state and is often capped at a specific amount. If you work in a profession with elevated litigation risk, such as medicine or business ownership, keeping funds in a 401(k) may offer stronger legal protection.

- You plan to retire between 55 and 59½. The Rule of 55 allows penalty-free withdrawals from a 401(k) after you separate from service at age 55 or later. IRAs do not offer this exception, and the 10% early withdrawal penalty applies until you reach 59½. Rolling over before you understand this distinction can lock you out of penalty-free access during a critical window.

- You have a Roth 401(k) and want to avoid creating a taxable event. Rolling a Roth 401(k) into a Roth IRA is straightforward and tax-free. But if your plan contains both pre-tax and Roth contributions, the rollover may need to be split across account types. Mishandling the split can create an unintended tax bill on the pre-tax portion.

Talk to a fee-only financial advisor before initiating any rollover. An independent professional can compare your current plan against IRA alternatives and identify whether rolling over improves or worsens your overall position.

Considering a Gold IRA Rollover?

If you are exploring Option 3 (roll to an IRA) and want to diversify beyond stocks and bonds, a Gold IRA rollover lets you hold physical precious metals inside a tax-advantaged retirement account. The process follows the same direct rollover mechanics described above: your old 401(k) custodian sends the funds directly to a self-directed IRA custodian, and no taxes are triggered.

A Gold IRA adds a layer of complexity that a standard IRA does not have. Think of it as upgrading from a regular car to one that requires specialty fuel — the driving is the same, but the maintenance costs and logistics are different. You need an IRS-approved custodian, an approved depository for storage, and metals that meet IRS fineness requirements. The fee structure is also different, with custodian fees, storage fees, and dealer markups all adding to the cost. Our Gold IRA hub is a good starting point for understanding whether this path fits your situation.

For a step-by-step walkthrough of how to move a 401(k) into physical gold, read our Gold IRA rollover overview. It covers custodian selection, the paperwork sequence, metal selection, and the specific mechanics of how Gold IRAs work once your funds arrive.

Whatever path you choose from The Four Options, the most important step is making an active decision rather than letting your old 401(k) sit forgotten. Even leaving the money in your old plan is a better outcome than cashing out. And if you decide to roll over, a direct trustee-to-trustee transfer is almost always the safest route.

James Hartley

Former financial journalist (8 years) · Series 65 license holder

James covers retirement planning and precious metals investing. He spent eight years as a financial journalist before joining PrizeMining to research Gold IRA providers, fee structures, and regulatory requirements.

Sources

Gold IRA Due Diligence Checklist

10 items to verify before you open an account: fee transparency, custodian credentials, storage terms, buyback policies, and more. Free PDF, straight to your inbox.

No spam. Unsubscribe anytime. We never share your email.

This content is for informational purposes only and does not constitute financial, investment, or tax advice. Gold IRAs carry risks including price volatility, limited liquidity, and fees that can erode returns. Always consult a qualified financial advisor before making retirement investment decisions.