IRA-Eligible Metals

Most gold and silver products are not IRA-eligible metals. The IRS requires gold to be 99.5% pure, silver 99.9%, and platinum and palladium 99.95%, as defined in IRS collectibles rules for IRAs. Buying the wrong product with IRA funds triggers an immediate taxable distribution plus a possible 10% penalty if you are under 59 and a half. This article lists every purity threshold, the one major exception, and how you can verify eligibility before you buy.

Over the past two years, we have catalogued more than 200 IRS-eligible coin and bar products and flagged the numismatic items most often misrepresented as IRA-eligible.

Key Takeaways

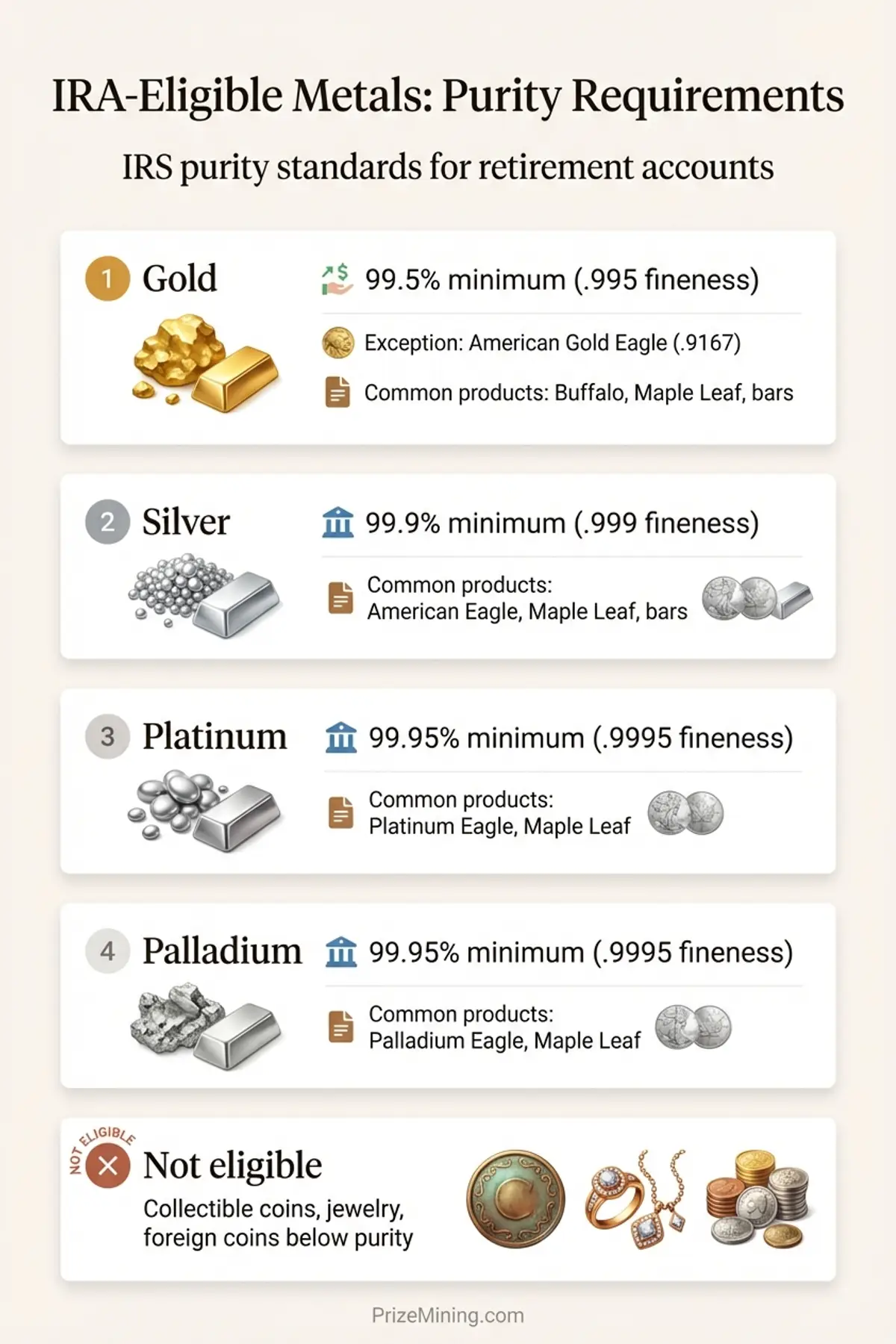

- Gold must be 99.5% pure, silver 99.9%, and platinum and palladium 99.95% to qualify for an IRA.

- The American Gold Eagle is the only exception — it is 91.67% pure but allowed by a special rule in the law.

- Collectible coins, jewelry, and products from non-accredited refiners are banned regardless of metal content.

What Are the IRS Purity Requirements?

The Purity Gate is a binary admit/reject test based on fineness rating. Each metal product must meet the IRS minimum threshold: 99.5% for gold (with statutory exceptions), 99.9% for silver, and 99.95% for platinum and palladium. Products falling short are rejected regardless of market value — a rare gold coin worth $50,000 at auction still fails if its purity is below the threshold (Source: 26 USC 408(m)(3)).

The IRS does not set a single purity standard for all metals. Each metal has its own minimum fineness, defined in the statute. The requirements below apply to any product purchased with IRA funds, whether held in a traditional IRA, Roth IRA, SEP IRA, or SIMPLE IRA.

Gold

| Requirement | Standard |

|---|---|

| Minimum fineness | 99.5% (0.995) |

| Statute | 26 USC 408(m)(3)(A)(ii) |

| Common eligible products | Canadian Gold Maple Leaf (99.99%), Austrian Gold Philharmonic (99.99%), gold bars from LBMA-accredited refiners |

| Notable exception | American Gold Eagle (91.67%) — allowed by separate statutory provision |

Silver

| Requirement | Standard |

|---|---|

| Minimum fineness | 99.9% (0.999) |

| Statute | 26 USC 408(m)(3)(A)(ii) |

| Common eligible products | American Silver Eagle (99.93%), Canadian Silver Maple Leaf (99.99%), Austrian Silver Philharmonic (99.9%), silver bars from LBMA/COMEX-approved refiners |

| Ineligible examples | Pre-1965 U.S. silver coins (90%), sterling silver items (92.5%) |

Platinum

| Requirement | Standard |

|---|---|

| Minimum fineness | 99.95% (0.9995) |

| Statute | 26 USC 408(m)(3)(A)(ii) |

| Common eligible products | American Platinum Eagle (99.95%), Canadian Platinum Maple Leaf (99.95%), platinum bars from NYMEX/COMEX-approved refiners |

Palladium

| Requirement | Standard |

|---|---|

| Minimum fineness | 99.95% (0.9995) |

| Statute | 26 USC 408(m)(3)(A)(ii) |

| Common eligible products | Canadian Palladium Maple Leaf (99.95%), palladium bars from NYMEX/COMEX-approved or LBMA-accredited refiners |

Knowing these purity thresholds is your first step. Your next question is what happens when a product looks like it should qualify but does not. If you want a broader look at precious metals and how they are priced, our precious metals resource center covers the fundamentals.

Why Is the American Gold Eagle an Exception?

The American Gold Eagle is 91.67% gold, 3% silver, and 5.33% copper. That is well below the 99.5% fineness threshold. By the standard purity rule, it should fail The Purity Gate. It does not, because Congress wrote a specific exception into the law.

Section 408(m)(3)(A)(i) of the Internal Revenue Code explicitly permits “gold coins described in paragraphs (7), (8), (9), and (10) of section 5112(a) of title 31.” Those paragraphs define the American Gold Eagle in its one-ounce, half-ounce, quarter-ounce, and tenth-ounce sizes. The Eagle gets its own line in the statute, separate from the general purity requirement (Source: 26 USC 408(m)).

The lesson we learned after months of reviewing IRS guidance: never assume a product qualifies based on metal content alone. The Eagle teaches you that IRA eligibility is a legal question, not a metallurgical one. A coin can contain a full troy ounce of pure gold and still be ineligible if Congress did not name it or if it fails the fineness test. Conversely, a coin can fall below the purity threshold and still qualify if it has a statutory carve-out. Always verify against the statute, not the product label (see the IRS Publication 590-A).

The American Gold Buffalo, by contrast, is 99.99% pure and qualifies under the standard fineness rule without needing any exception. If you want to understand how the premiums on these coins compare to their underlying metal value, our spot price vs premium article breaks down that relationship.

Which products are approved and which are prohibited?

The difference between IRA-eligible gold and collectible gold coins is one of the most common points of confusion in precious metals investing. Both are gold. Both have real market value. But the IRS treats them completely differently inside a retirement account. Buying a collectible coin with IRA funds triggers an immediate taxable distribution under Section 408(m)(1), as if you withdrew cash from your IRA and spent it. The tax bill arrives whether you intended to make a distribution or not (Source: IRS).

Think of it like a building code inspection. Two houses can look identical from the street, but one passes inspection and the other fails because it does not meet the structural requirements hidden inside the walls. Collectible gold coins may look the same as bullion coins to a casual buyer, but they fail the IRS inspection because they do not meet the purity or statutory requirements built into the tax code.

| Product | IRA Status | Reason |

|---|---|---|

| American Gold Eagle (1 oz) | Approved | Statutory exception under 408(m)(3)(A)(i) |

| American Gold Buffalo (1 oz) | Approved | 99.99% pure — exceeds 99.5% minimum |

| Canadian Gold Maple Leaf | Approved | 99.99% pure — exceeds 99.5% minimum |

| Austrian Gold Philharmonic | Approved | 99.99% pure — exceeds 99.5% minimum |

| PAMP Suisse gold bar (1 oz) | Approved | 99.99% pure, LBMA-accredited refiner |

| American Silver Eagle | Approved | 99.93% pure — meets 99.9% silver minimum |

| South African Krugerrand | Prohibited | 91.67% pure — no statutory exception |

| Pre-1933 U.S. gold coins | Prohibited | Classified as collectibles under 408(m)(2) |

| British Gold Sovereign | Prohibited | 91.67% pure — no statutory exception |

| Gold jewelry (any karat) | Prohibited | Not bullion — classified as collectible |

| Pre-1965 U.S. silver coins | Prohibited | 90% silver — below 99.9% minimum |

The Krugerrand is an instructive case. It contains exactly one troy ounce of gold and is 91.67% pure — identical to the American Gold Eagle on both metrics. The two coins differ only in legal status under IRC § 408(m)(3): the Eagle has a statutory exception that admits sub-99.5% purity coins; the Krugerrand has no such exception. Buying a Krugerrand with IRA funds would be treated as a taxable distribution. Understanding how a Gold IRA works from the start helps you avoid purchasing products that trigger unexpected tax consequences.

Which Mints and Refiners Are Approved?

Purity alone does not guarantee IRA eligibility for the product you want to buy. The tax code also requires that bars and rounds be produced by a manufacturer accredited by NYMEX, COMEX, or a national government mint. For gold specifically, bars must also meet the standards of an LBMA-accredited refiner. This requirement exists to ensure your product can be independently verified and is not counterfeit (Source: 26 USC 408(m)(3)(B); LBMA).

Think of LBMA accreditation as a diploma hanging on the wall. A refiner without it may produce perfectly fine gold, but the IRS will not accept the product into your IRA without the credential. The accreditation process involves independent assay testing, facility inspections, and ongoing compliance monitoring. It is the manufacturing equivalent of passing The Purity Gate.

Commonly accepted mints and refiners

- Government mints: U.S. Mint, Royal Canadian Mint, Perth Mint (Australia), Austrian Mint, Royal Mint (UK)

- LBMA-accredited refiners (gold): PAMP Suisse, Valcambi, Heraeus, Argor-Heraeus, Metalor, Johnson Matthey

- COMEX/NYMEX-approved (silver, platinum, palladium): Most of the LBMA refiners above, plus Engelhard, Asahi Refining, and Republic Metals

Before purchasing bars for an IRA, confirm two things: the fineness meets the statutory minimum, and the manufacturer appears on the current LBMA Good Delivery List or is a COMEX/NYMEX-approved refiner. Custodians like STRATA Trust maintain their own accepted product lists, and a bar from an unrecognized refiner will be rejected at the depository regardless of its purity (Source: STRATA Trust).

What Mistakes Lead to Non-Eligible Purchases?

Most eligibility errors happen before the investor contacts a custodian. Buying non-eligible metals for an IRA is like purchasing luggage that does not fit in the overhead bin — you find out too late, and the cost of fixing it falls on you. A dealer recommends a product, the investor assumes it qualifies, and the problem surfaces weeks later when the depository refuses to accept it or the custodian flags it as a collectible. At that point, the IRS may treat the purchase as a taxable distribution, and if the investor is under 59 and a half, a 10% early withdrawal penalty may apply on top of the income tax (Source: IRS Publication 590-A).

- Buying “rare” or “numismatic” coins for an IRA. Some dealers push rare coins because their markups are dramatically higher, often 30% to 50% above melt value. These coins are classified as collectibles and are explicitly prohibited. A dealer who recommends numismatic coins for an IRA is either uninformed or prioritizing their commission. Our Gold IRA scams overview covers this tactic in detail.

- Assuming all gold coins qualify. The Krugerrand, British Sovereign, and French 20 Franc are all real gold coins with active secondary markets. None of them meet the IRA purity requirement, and none have a statutory exception. Gold content does not equal IRA eligibility.

- Buying bars from unaccredited refiners. A 99.99% gold bar from a refiner not on the LBMA Good Delivery List will be rejected by most custodians. The purity may be genuine, but without the accreditation, the bar cannot be independently verified to the standard the IRS requires.

- Confusing “proof” coins with collectible coins. A proof version of an American Gold Eagle is IRA-eligible because the underlying coin qualifies by statute. A proof version of a non-eligible coin remains non-eligible. The proof designation does not change the purity or the legal status of the base product.

- Holding metals at home. Even if you buy the right products, storing them in a home safe or a personal bank safe deposit box disqualifies the investment. IRA metals must be held by an IRS-approved depository. The how a Gold IRA works page explains the custody chain in detail.

How can you verify a product's IRA eligibility?

Verifying eligibility before you buy is far cheaper than discovering a problem after the purchase. The process takes a few minutes and eliminates the risk of a taxable distribution triggered by an ineligible product. Follow these steps in order.

1. Check the fineness against the statutory minimum

Confirm the product's purity: 99.5% for gold, 99.9% for silver, 99.95% for platinum and palladium. The fineness is usually stamped on the product or listed on the mint's official specification sheet. If the product is an American Gold Eagle, it qualifies regardless of fineness through the statutory exception.

2. Verify the manufacturer's accreditation

For bars, confirm the refiner appears on the current LBMA Good Delivery List or is NYMEX/COMEX-approved. For coins, confirm the issuing mint is a recognized national government mint. The LBMA publishes its current list online and updates it regularly (Source: LBMA).

3. Cross-reference with your custodian's approved product list

Most IRA custodians maintain a list of pre-approved products. Even if a product meets the statutory requirements, your specific custodian may not accept it. Ask your custodian to confirm in writing that the product you plan to purchase is eligible and will be accepted at their depository. STRATA Trust, for example, publishes a detailed precious metals reference listing accepted products (Source: STRATA Trust).

4. Get written confirmation before placing the order

Request an email or written statement from both the dealer and the custodian confirming the product's eligibility. If the product is later rejected, this documentation protects you. A verbal assurance from a salesperson is not enforceable and will not help with the IRS. Understanding the full cost structure of your purchase, including markups on specific eligible products, is equally important before you commit.

When to Choose a Specific Metal Type

- Coin premium vs bar premium matters to you — if you want the lowest entry premium, 1 oz LBMA-accredited gold bars typically cost 2% to 5% over spot, while coins run 4% to 10%.

- Liquidity needs drive your choice — if you anticipate partial liquidations, smaller denominations like 1/10 oz Gold Eagles let you sell in smaller slices without releasing your entire position.

- Storage preferences influence product selection — if your depository charges by weight or dimension, compact high-purity bars take less space than equivalent coin holdings and may reduce your annual storage bill.

When to Talk to a Financial Advisor

Consider consulting a fee-only financial advisor before proceeding if any of these apply to your situation:

- A dealer is recommending products you cannot verify as IRA-eligible

- You want to confirm that a specific coin or bar meets IRS purity requirements

- You are considering non-standard metals and need guidance on eligibility

How do you go from eligibility to execution?

Knowing which metals qualify is the starting point. The next steps involve choosing a custodian, funding the account, selecting specific products, and ensuring they reach an approved depository in the correct form. Each step has its own requirements and potential pitfalls.

Our how a Gold IRA works overview walks through the entire process from opening an account to receiving your first depository statement. If you are concerned about the cost side, the Gold IRA fees breakdown shows exactly what you will pay at each stage. And if someone is pressuring you to buy quickly without explaining eligibility, the scams overview explains why that pressure is itself a warning sign.

For broader context on precious metals beyond IRA investing, including how spot prices relate to what you actually pay, our spot price vs premium article explains the gap between the quoted price and the real purchase cost. The Gold IRA resource center connects all of our articles, tools, and provider research in one place.

The Purity Gate is strict by design. The IRS built these requirements to keep collectibles, jewelry, and substandard products out of tax-advantaged retirement accounts. Investors who understand the gate before they shop avoid costly mistakes. Those who do not often discover the rules only after a rejected deposit or an unexpected tax bill.

James Hartley

Former financial journalist (8 years) · Series 65 license holder

James covers retirement planning and precious metals investing. He spent eight years as a financial journalist before joining PrizeMining to research Gold IRA providers, fee structures, and regulatory requirements.

Sources

Gold IRA Due Diligence Checklist

10 items to verify before you open an account: fee transparency, custodian credentials, storage terms, buyback policies, and more. Free PDF, straight to your inbox.

No spam. Unsubscribe anytime. We never share your email.

This content is for informational purposes only and does not constitute financial, investment, or tax advice. Gold IRAs carry risks including price volatility, limited liquidity, and fees that can erode returns. Always consult a qualified financial advisor before making retirement investment decisions.