Gold IRA vs Traditional IRA — Key Differences Explained

A Gold IRA and a Traditional IRA are built on the same IRS framework but solve different problems. Both accounts follow identical contribution limits under 26 U.S. Code 408, yet Gold IRA fees run 10 to 30 times higher than a typical Traditional IRA at a mainstream brokerage (Source: Yahoo Finance). That gap can erase decades of compounding if you pick the wrong wrapper for the wrong goal. This article walks you through what we call The IRA Asset Divide — the choice between paper-asset accounts and physical-asset accounts. You will see tax mechanics, fee comparisons, liquidity trade-offs, and a clear view of when each fits.

Since 2024, we have reviewed more than 15 Gold IRA provider fee schedules alongside the expense ratios of 20+ major Traditional IRA custodians to quantify the cost gap shown throughout this page.

Key Takeaways

- A Gold IRA holds physical precious metals; a Traditional IRA typically holds stocks, bonds, and mutual funds.

- Both accounts follow the same IRS tax rules, contribution limits, and distribution rules.

- Gold IRAs cost 10 to 30 times more per year and are less liquid, so they usually work best as a small piece of a broader retirement plan.

What is the key difference between a Gold IRA and a Traditional IRA?

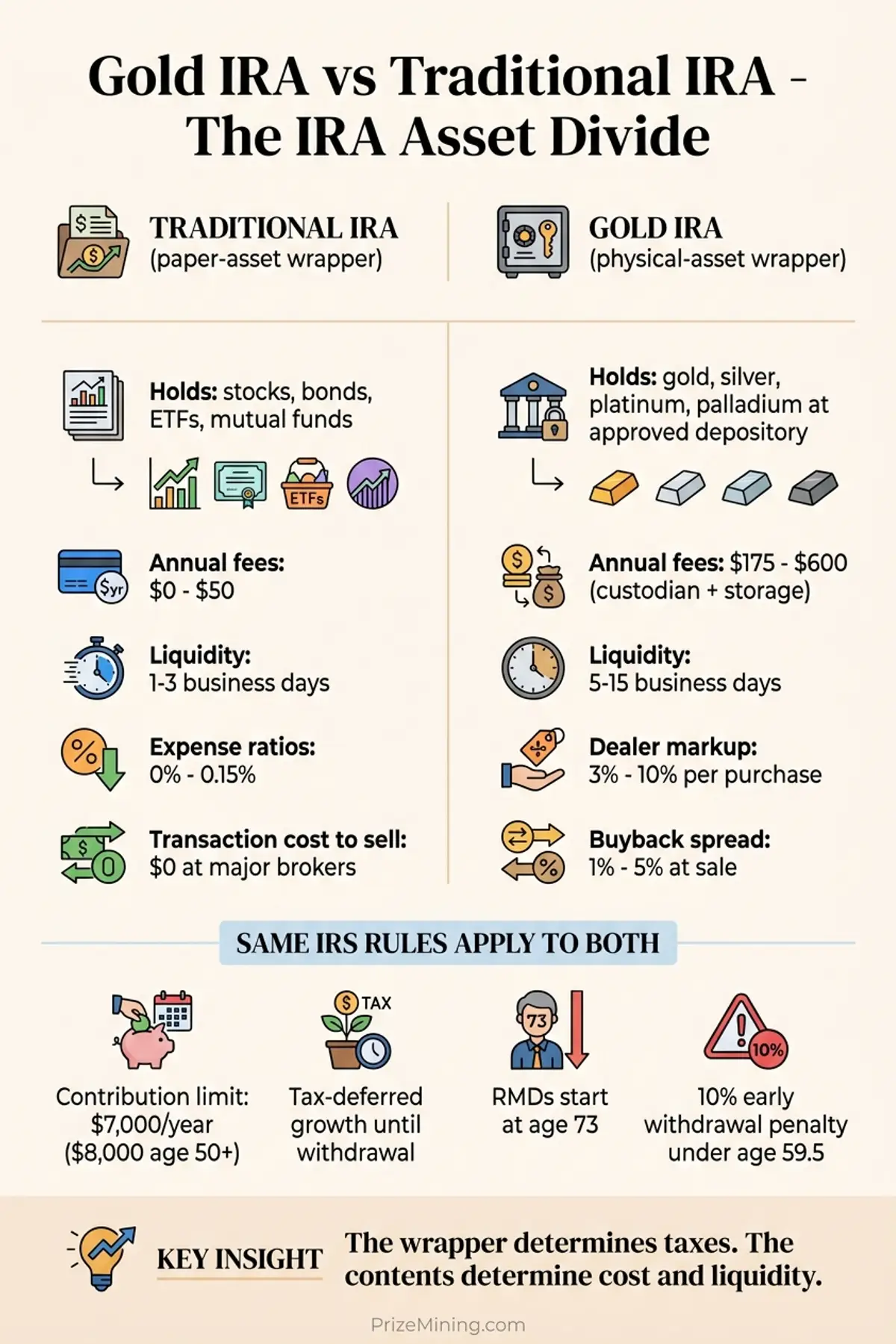

The difference between a Gold IRA and a Traditional IRA is what each account can hold. A Traditional IRA at a brokerage like Fidelity, Schwab, or Vanguard holds publicly traded securities — stocks, bonds, ETFs, and mutual funds. A Gold IRA is a self-directed IRA configured to hold physical precious metals at an IRS-approved depository (Source: IRS FAQs on IRAs).

Both accounts sit under the same tax law. Both use the same contribution limits. Both allow rollovers from 401(k)s and other qualified plans. The wrapper — the legal structure around your retirement assets — is nearly identical. What you can buy inside the wrapper is where the accounts diverge. That is The IRA Asset Divide: paper assets on one side, physical assets on the other.

A Traditional IRA at a brokerage operates with instant trades and low operational friction (one click, T+2 settlement). A Gold IRA operates with multi-day workflows: every buy or sell requires custodian instructions, depository coordination, and dealer transactions — typical timelines of 5–14 business days for a sell, 7–14 for a buy. The contents are real and physical, but every move involves paperwork, shipping, and storage costs.

You can read how the Gold IRA structure works end to end in our five-step Gold IRA overview, which maps the four parties involved in every Gold IRA: custodian, dealer, depository, and account owner.

Note: Confusion Entity

A Gold IRA is not the same as holding a gold ETF inside a Traditional IRA. A Gold IRA holds physical metal at a depository. A gold ETF is a paper security that tracks the metal's price and trades on a stock exchange. Same exposure to gold prices, very different cost and liquidity profile.

How do tax rules compare side-by-side?

Gold IRAs and Traditional IRAs follow identical tax rules under IRS Publication 590-A and 590-B. The wrapper determines your taxes, not the assets inside it (Source: IRS Publication 590-A).

| Tax Rule | Traditional IRA | Gold IRA |

|---|---|---|

| Contribution limit (2026, under 50) | $7,000/year | $7,000/year |

| Catch-up contribution (50+) | $1,000/year | $1,000/year |

| Tax treatment of contributions | Tax-deductible (if eligible) | Tax-deductible (if eligible) |

| Tax on growth | Deferred until withdrawal | Deferred until withdrawal |

| Withdrawals taxed as | Ordinary income | Ordinary income |

| Early withdrawal penalty (under 59½) | 10% | 10% |

| Required minimum distributions | Start at age 73 | Start at age 73 |

One practical difference sits inside the RMD rule. A Traditional IRA custodian can sell a fraction of an index fund and cut you a check. A Gold IRA custodian has to sell physical metal or ship it to you as an in-kind distribution, which adds days to the process and can trigger dealer buyback spreads. Our RMD rules overview covers the mechanics of both paths.

The contribution limit applies across all of your IRAs combined — not per account. Opening a Gold IRA alongside a Traditional IRA does not double your annual contribution room (Source: 26 U.S. Code § 408).

What does each account hold?

A Traditional IRA at a mainstream brokerage holds paper assets that trade on public exchanges. A Gold IRA holds physical metals in a vault. That asset difference cascades into everything else: fees, liquidity, storage, and how you take money out.

Traditional IRA — What You Can Own

- Publicly traded stocks and bonds

- Mutual funds and ETFs (including gold ETFs like GLD and IAU)

- Target-date retirement funds

- Certificates of deposit and Treasury bills

- Money market funds

Gold IRA — What You Can Own

- Gold bullion at 99.5% purity or higher (with the American Gold Eagle as a statutory exception)

- Silver bullion at 99.9% purity

- Platinum and palladium at 99.95% purity

- Specific IRS-approved coins from sovereign mints

The Gold IRA eligibility rules are strict. Collectible coins, rare numismatics, and jewelry are prohibited under 26 U.S. Code § 408(m) and buying them with IRA funds triggers a full taxable distribution. See the IRA-eligible metals reference for the exact purity standards and product list.

How do fees compare at a glance?

Gold IRA fees are significantly higher than Traditional IRA fees. A mainstream brokerage Traditional IRA typically costs 0% to 0.15% per year in expense ratios on index funds, with no account maintenance fee. A Gold IRA layers setup fees, annual custodian fees, storage fees, and dealer markups on top of whatever the metals appreciate (Source: Yahoo Finance).

| Fee Type | Traditional IRA | Gold IRA |

|---|---|---|

| Setup fee | $0 | $50 – $200 |

| Annual account fee | $0 | $75 – $300 |

| Storage & insurance | Not applicable | $100 – $300/year |

| Expense ratio on holdings | 0% – 0.15% (index funds) | Not applicable |

| Dealer markup (one-time) | Not applicable | 3% – 10% above spot |

| Typical 5-year cost on $100K | ~$500 – $750 | ~$4,875 – $13,200 |

On a $100,000 account over five years, a Gold IRA costs roughly 10 to 30 times more than a Traditional IRA at a mainstream brokerage. That cost difference is not a flaw — it reflects the real expense of storing, insuring, and handling physical metal. But it has to be weighed against what you expect the metal to do for your portfolio. Our Gold IRA fee estimator projects the total cost across different account sizes and time horizons.

What liquidity and access trade-offs apply?

A Traditional IRA is highly liquid. You can sell an index fund during market hours and have cash available within 1 to 3 business days. A Gold IRA is much less liquid. Selling metals requires coordinating with the depository, the dealer, and the custodian, which typically takes 5 to 15 business days (Source: Investopedia).

The liquidity gap matters most near retirement. Required minimum distributions, unexpected medical costs, and portfolio rebalancing all become harder when your assets need a buyer and a shipping process before they convert to cash. Our Gold IRA liquidation overview walks through both exit paths — cash settlement and physical in-kind distribution.

| Access Scenario | Traditional IRA | Gold IRA |

|---|---|---|

| Sell and receive cash | 1 – 3 business days | 5 – 15 business days |

| Transaction cost to sell | $0 at major brokers | 1% – 5% buyback spread |

| Partial rebalancing | Same day, fractional | Whole coins or bars only |

| In-kind distribution | Shares transferred electronically | Physical metals shipped to home |

When does a Gold IRA make more sense than a traditional IRA?

A Gold IRA makes more sense than a traditional IRA in three specific situations: portfolio size of $100,000 or more (fee drag becomes manageable), a defined diversification mandate of 5–10% precious-metals allocation (modest size limits the cost), and time horizon of 10 years or longer (gives appreciation time to absorb the dealer markup). Outside those conditions, a traditional IRA delivers similar retirement outcomes at lower cost.

- You want a small physical-metals allocation. A 5 to 10 percent Gold IRA position alongside a larger Traditional IRA gives you diversification without concentrating fees or volatility.

- Your retirement plan already has paper-asset exposure. A Traditional IRA full of stocks and bonds benefits from a non-correlated asset; a Gold IRA can supply that without changing the core plan.

- You have a long time horizon. With 10 or more years until retirement, fixed Gold IRA fees have time to be absorbed by potential metal appreciation.

- Your account size is $50,000 or more. Below $50,000, fixed annual fees eat 1 to 2 percent of the balance every year before any dealer markup — making the math difficult to justify.

When is a traditional IRA the better fit?

For most retirement savers, a Traditional IRA at a mainstream brokerage is the better default. It is cheaper, simpler, more liquid, and supports automatic investment strategies that Gold IRAs cannot match.

- You want low-cost diversified exposure. A single total-market index fund inside a Traditional IRA gives you thousands of companies at a 0.03 percent expense ratio. No Gold IRA can match that.

- You plan to dollar-cost average. Traditional IRAs let you add small amounts monthly without transaction fees. Gold IRAs charge a dealer markup on every new metal purchase.

- You want simple required minimum distributions. Selling fractions of an index fund to meet an RMD is straightforward. Shipping physical metal or liquidating coins at dealer buyback spreads adds cost and complexity.

- Fixed annual fees hit smaller accounts much harder. On retirement savings under $50,000, Gold IRA fees consume 1 to 2 percent per year before any dealer markup. A Traditional IRA with no account minimum avoids that drag.

If you are considering a Gold IRA despite falling into this group, our Gold IRA risks overview covers the specific downsides that matter most for smaller or more conservative portfolios.

Can you hold both a Gold IRA and a Traditional IRA?

Yes. You can hold a Gold IRA and a Traditional IRA at the same time. The IRS treats them as separate accounts for administrative purposes, but a single combined contribution limit applies across both (Source: 26 U.S. Code § 408). Many investors use this structure on purpose: a core Traditional IRA for low-cost diversified growth and a smaller Gold IRA for physical-metal diversification.

A rollover between the two is tax-free when done as a direct trustee-to-trustee transfer. You can move part of a Traditional IRA balance into a new Gold IRA without triggering taxes or penalties, as long as the metals go directly to an IRS-approved depository. The Gold IRA rollover process covers the paperwork and timing for this kind of partial move.

What are the most common mistakes when choosing?

The mistakes we see most often stem from investors treating a Gold IRA and a Traditional IRA as interchangeable when they are not. Early in our research in 2024, we expected fee drag to be the dominant hidden cost. After reviewing 15+ provider schedules alongside liquidation complaints, we found that dealer buyback spreads at distribution time often cost more than multiple years of account fees combined. That changed how we weigh the two account types for investors nearing retirement.

- Rolling over a full Traditional IRA into a Gold IRA. This concentrates fees, volatility, and liquidity risk into a single asset class. Most planners recommend keeping the Gold IRA to 5 to 10 percent of total retirement assets.

- Assuming the contribution limit doubles. Opening a second IRA does not give you a second $7,000 contribution room. The limit applies in total across all IRAs.

- Taking possession of Gold IRA metals. Moving metals from the depository to your home triggers a full taxable distribution and a 10 percent penalty if you are under 59 and a half. Our home storage Gold IRA overview covers why this fails.

- Ignoring dealer markups. A Gold IRA fee schedule showing $250 per year in custodian and storage costs looks cheap until you realize the dealer markup on the initial purchase can be 5 percent of the account balance.

- Using a Gold IRA for RMDs without a liquidation plan. Required minimum distributions at age 73 need actual cash. Selling metals adds days to the process and buyback spreads cut into the payout.

What Does the Research Show?

Academic work on gold's role in retirement portfolios consistently shows two things. First, gold has low long-run correlation with US equities, which supports its use as a diversifier. Second, gold's real return over 40-plus years is close to zero once fees and storage costs are included, meaning it is a stabilizer rather than a growth engine (Source: Investopedia).

The limitation: most studies compare gold to stock portfolios, not gold-inside-an-IRA-wrapper to stocks-inside-an-IRA-wrapper. Our own provider review suggests that Gold IRA fees shift the break-even point — a gold allocation that would work in a brokerage account may not work inside a high-fee IRA wrapper. Keep that fee wedge in mind when applying portfolio research to your own plan.

When Should You Talk to a Specialist?

The Gold IRA versus Traditional IRA decision often requires more than a self-research process. A fee-only CERTIFIED FINANCIAL PLANNER™ or tax professional can evaluate your full situation in ways a comparison article cannot.

- You are considering moving more than 15 percent of your retirement savings into a Gold IRA. Concentration risk at that level changes the conversation from diversification to speculation.

- You are near or in retirement and planning RMDs. The liquidity gap between Gold IRA and Traditional IRA becomes more expensive as you approach age 73.

- You have a complex rollover. Inherited IRAs, Roth conversions, and multi-employer 401(k) consolidations all interact differently with a self-directed Gold IRA structure.

- You are evaluating a high-pressure sales pitch. Any Gold IRA provider pushing a rollover with urgency tactics should be a signal to pause and consult an independent professional. See our Gold IRA scams overview for the specific red flags.

Frequently Asked Questions

Can I convert my Traditional IRA to a Gold IRA?

Yes. You can roll over some or all of a Traditional IRA into a self-directed IRA that holds physical precious metals. A direct trustee-to-trustee transfer is tax-free. The Gold IRA must be held by an IRS-approved custodian, and the metals must be stored in an approved depository — not at home.

Do Gold IRAs have the same contribution limits as Traditional IRAs?

Yes. Both account types follow the same IRS contribution limits under 26 U.S. Code 408. For 2026, that is $7,000 per year, or $8,000 if you are age 50 or older. The limit applies across all of your IRAs combined, not per account.

Are Gold IRAs riskier than Traditional IRAs?

Different, not universally riskier. Traditional IRAs face market risk on stocks and bonds. Gold IRAs face four distinct risk categories: gold price volatility (multi-year flat or declining periods historically), higher fees that erode returns (3–13% first year), lower liquidity (5–14 day sale processes), and scam exposure from the unregulated dealer market (Source: SEC Investor Alert). The risk profile depends on how each account is used and what it holds.

Should I replace my Traditional IRA with a Gold IRA?

Most financial planners recommend against replacing a diversified Traditional IRA with a Gold IRA. A Gold IRA tends to work better as a small allocation within a broader retirement plan, typically 5 to 10 percent of total retirement assets. Replacing a core IRA removes diversification and concentrates fees and volatility in a single asset class.

The Bottom Line

The IRA Asset Divide is the shortest way to understand the choice. A Traditional IRA is a paper-asset wrapper built for low-cost, liquid, diversified exposure. A Gold IRA is a physical-asset wrapper built for a specific diversification role — held at higher cost, stored in a vault, and traded through a slower settlement process. Both are legitimate retirement tools when used for the job they fit.

For most investors, that means keeping a Traditional IRA as the core retirement account and adding a Gold IRA only as a small, intentional allocation. If you are weighing that allocation, start with the Gold IRA fees breakdown to see the true all-in cost, then check the Gold IRA risks overview to understand what you are trading for the diversification. Before committing, a session with a fee-only advisor is worth more than any calculator.

James Hartley

Former financial journalist (8 years) · Series 65 license holder

James covers retirement planning and precious metals investing. He spent eight years as a financial journalist before joining PrizeMining to research Gold IRA providers, fee structures, and regulatory requirements.

Sources

Gold IRA Due Diligence Checklist

10 items to verify before you open an account: fee transparency, custodian credentials, storage terms, buyback policies, and more. Free PDF, straight to your inbox.

No spam. Unsubscribe anytime. We never share your email.

This content is for informational purposes only and does not constitute financial, investment, or tax advice. Gold IRAs carry risks including price volatility, limited liquidity, and fees that can erode returns. Always consult a qualified financial advisor before making retirement investment decisions.