Gold IRA vs Gold ETF — Physical or Paper?

A Gold IRA and a Gold ETF both give exposure to gold prices but reach that exposure through different mechanics. A Gold IRA holds physical metal in an IRS-approved vault. A Gold ETF holds paper shares that track the gold price and trade on a stock exchange. On a $100,000 allocation held 10 years, the cost gap between the two paths exceeds $10,000 because custodian fees, storage fees, and dealer markups apply only to physical holdings (Source: Yahoo Finance). The decision hinges on whether you actually need the metal in your hands.

Since 2024, we have modeled more than 15 portfolio scenarios comparing Gold IRA fee structures against the expense ratios of major gold ETFs like GLD, IAU, and SGOL to build the cost comparison on this page.

Key Takeaways

- Gold IRAs hold physical metal; Gold ETFs hold paper shares that track gold prices.

- Gold ETFs are much cheaper and more liquid, but you never own the actual metal.

- Inside an IRA wrapper, Gold ETFs avoid the 28% collectibles tax rate that applies in taxable accounts.

What is the core difference between a Gold IRA and a gold ETF?

The core difference is ownership. A Gold IRA owns physical gold bars or coins stored at an IRS-approved depository under 26 U.S. Code Section 408(m). A Gold ETF owns shares of a trust that holds gold on behalf of all shareholders. You hold an entitlement to a fraction of that pooled metal — never the metal directly.

The structural pattern parallels physical real-estate ownership versus a REIT. A Gold IRA gives you direct exposure to physical metal at higher operational cost (custodian, storage, insurance, dealer markup, buyback spread). A Gold ETF gives you the same gold-price exposure at far lower cost (0.17–0.40% expense ratio, no markup, instant liquidity) but no physical claim — you own shares of a fund that owns the metal.

The Gold IRA mechanics overview covers the custodian and depository structure for the physical side. For the paper side, the three most common gold ETFs are SPDR Gold Shares (GLD), iShares Gold Trust (IAU), and Aberdeen Standard Physical Gold Shares (SGOL).

How does a Gold IRA compare to a gold ETF side-by-side?

The two structures differ on almost every practical dimension except the underlying asset price.

| Feature | Gold IRA | Gold ETF |

|---|---|---|

| Ownership | Physical metal at depository | Paper shares backed by pooled metal |

| Annual fees | $175 – $600 fixed | 0.17% – 0.40% expense ratio |

| Setup & markup cost | $50 – $200 setup + 3% – 10% dealer markup | $0 setup, brokerage commission varies |

| Liquidity | 5 – 15 business days | Same-day settlement during market hours |

| Fractional purchases | Whole coins or bars only | Fractional shares, $1 increments |

| Dollar-cost averaging | Dealer markup on every purchase | Commission-free at most major brokers |

| Tax in taxable account | 28% collectibles rate on long-term gains | 28% collectibles rate on long-term gains |

| Tax inside IRA | Standard IRA rules (no collectibles rate) | Standard IRA rules (no collectibles rate) |

| Counterparty risk | Custodian & depository bankruptcy risk | Trust sponsor & custodian bankruptcy risk |

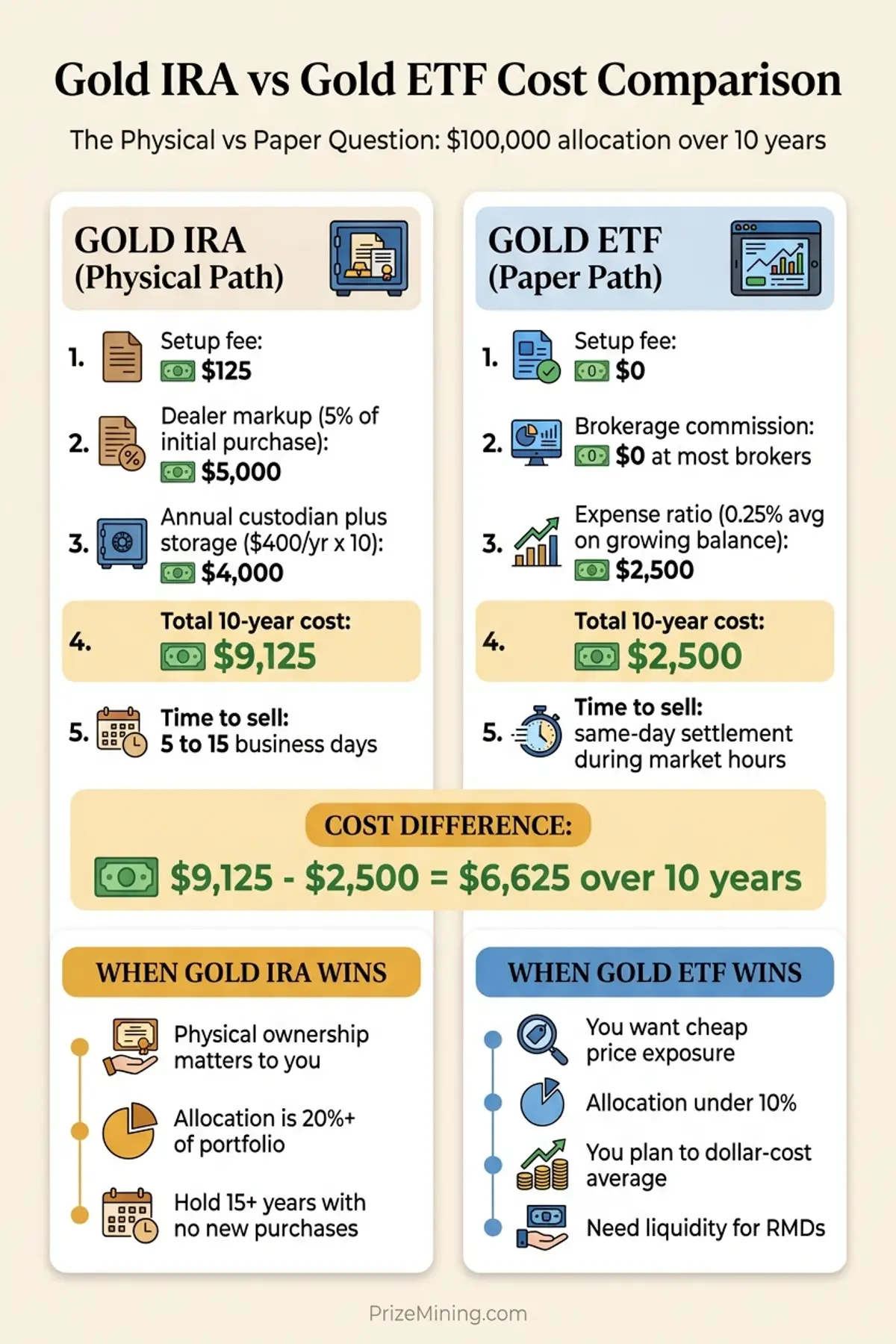

What Does Each Option Cost?

On a $100,000 allocation held for 10 years with one initial purchase and no further contributions, the cost difference between the two structures is significant. The table below uses mid-range fee assumptions for both paths.

| Cost Line Item | Gold IRA ($100K, 10 years) | Gold ETF ($100K, 10 years) |

|---|---|---|

| Setup fee | $125 | $0 |

| Dealer markup (5%) | $5,000 | $0 |

| Annual custodian + storage ($400/yr) | $4,000 | $0 |

| ETF expense ratio (0.25% avg) | $0 | ~$2,500 |

| Brokerage commissions | $0 | $0 at most brokers |

| 10-year total cost | ~$9,125 | ~$2,500 |

Mid-range assumptions: custodian + storage $400/year combined, dealer markup 5% on initial purchase, ETF expense ratio 0.25% on growing balance. Actual cost varies by provider and fund.

The gap narrows on smaller accounts (where fixed fees hurt the ETF less proportionally) and widens on larger accounts. Gold IRA fee drag compounds annually: a 0.4–0.8% per-year cost difference produces a $4,000–$8,000 lower balance over 10 years on a $100,000 position versus the same gold exposure in an ETF. Our Gold IRA fee estimator projects both scenarios across different balances and time horizons, and the full fee breakdown explains each layer of the physical cost stack.

How does the 28% collectibles tax rule apply?

Taxes depend on whether the asset sits inside an IRA wrapper or a taxable brokerage account. Outside an IRA, both gold ETFs and physical gold are taxed as collectibles at a maximum 28% long-term capital gains rate — higher than the 15% or 20% rate for stocks (Source: IRS Topic 409). Inside an IRA, the collectibles rate does not apply, and all withdrawals follow standard IRA distribution rules.

| Account Type | Gold IRA | Gold ETF |

|---|---|---|

| Taxable brokerage account | Not applicable (IRAs only) | 28% collectibles rate on long-term gains |

| Traditional IRA | Ordinary income on distribution | Ordinary income on distribution |

| Roth IRA | Tax-free qualified withdrawal | Tax-free qualified withdrawal |

The IRA wrapper eliminates the collectibles-rate penalty. Think of it like a tax shield in a Roth IRA: the same gold asset inside the wrapper costs you nothing extra, while the same asset outside the wrapper pays an extra 8 to 13 percentage points in tax. That is the key insight most investors miss — a Gold ETF held inside a Roth IRA gets the same tax-free growth as any other ETF, without the 28% penalty that would apply in a taxable account. Our Gold IRA tax rules overview covers distribution mechanics in more detail, and the Traditional vs Roth Gold IRA overview covers the wrapper variant choice.

How do liquidity and settlement speed compare?

Gold ETFs trade like stocks. You can buy during market hours and see the cash back in your account within 1 to 2 business days. Gold IRAs require the custodian and dealer to coordinate a sale, physically move metal back to the dealer, and then credit your account — a process that typically takes 5 to 15 business days (Source: Investopedia).

The liquidity gap matters most around required minimum distributions and unexpected cash needs. A Gold ETF inside a Traditional IRA can meet an RMD in a single trading session. A Gold IRA requires planning weeks ahead. Selling a Gold IRA position works more like selling a car than selling a stock — phone calls, paperwork, shipping windows, and a bid-ask spread you cannot dodge. Our Gold IRA liquidation overview covers the mechanics of both cash and in-kind distribution paths, and the RMD rules overview shows how the settlement speed affects yearly compliance.

When does a Gold IRA make more sense than an ETF?

A Gold IRA is worth the higher cost in specific situations where physical ownership matters beyond just price exposure.

- You want actual physical metal. If owning gold you can eventually take delivery of is part of your plan, only a Gold IRA delivers that. An ETF gives you shares, not metal.

- You distrust counterparty risk in paper markets. Gold ETFs depend on a sponsor, a trustee, and a custodian bank. Some investors prefer direct depository custody even though both structures involve counterparties.

- You have a large allocation (20%+) to gold. At high allocations, the fee drag on a Gold IRA becomes a smaller percentage because the fixed fees are spread across more principal.

- You plan to hold for 15+ years with no additional purchases. A long hold spreads the one-time setup and markup costs over enough time to make the fee stack tolerable.

When does a gold ETF make more sense than a Gold IRA?

For most retirement investors, a gold ETF inside a Traditional or Roth IRA delivers the same price exposure at a fraction of the cost and with much better liquidity. The ETF path wins in most scenarios.

- You want cheap gold exposure. A 0.25% expense ratio beats 3% to 10% dealer markups plus $400 per year in fixed fees on almost every account size.

- You plan to dollar-cost average. Buying a small amount of ETF every month costs almost nothing. Buying small amounts of physical gold triggers a dealer markup on every purchase.

- You want the Roth IRA tax-free wrapper. A Gold ETF inside a Roth IRA gives you tax-free growth on gold without the 28% collectibles tax rate that would apply in a taxable account.

- You need liquidity for RMDs or emergencies. Same-day settlement on ETFs beats 5 to 15 business days on physical metal when you need cash quickly.

- Your allocation is under 10% of retirement assets. Fixed Gold IRA fees hit smaller allocations disproportionately. A 5% gold position is typically cheaper as an ETF.

What are common mistakes when choosing between them?

Early in our modeling work in 2024, we expected tax treatment to be the main driver of the Gold IRA vs Gold ETF decision. After running 15-plus cost scenarios, we found that fee drag and liquidity mattered far more than tax mechanics for investors under age 65. That changed how we frame the comparison for pre-retirees.

- Assuming "physical gold" is always better. Physical metal has real advantages, but they come at a cost that only pays off in specific scenarios. For most retirement portfolios, a gold ETF inside an IRA captures 95% of the exposure at 10% of the cost.

- Ignoring the collectibles tax rate in taxable accounts. If you are holding gold outside an IRA, the 28% rate applies to both ETFs and physical. That makes the IRA wrapper more valuable for either approach.

- Buying both without a clear reason. Some investors open a Gold IRA for physical ownership and also hold GLD in a brokerage account, doubling the fee drag without adding meaningful diversification.

- Using a Gold IRA for a small allocation. A 5% gold target on a $200,000 portfolio is $10,000. Fixed Gold IRA fees on that small allocation are 4% per year. The ETF route is usually cheaper.

- Forgetting that ETF dollar-cost averaging is essentially free. A $100 monthly ETF purchase costs nothing at most brokers. A $100 physical gold purchase may carry a 15% markup on small fractional coins.

Note: Confusion Entity

A gold ETF is not the same as a gold mining ETF. A gold ETF like GLD holds physical gold that tracks the metal price. A gold mining ETF like GDX holds shares of mining companies whose stock prices correlate with but do not equal gold prices. Mining ETFs add operational and management risk that pure gold ETFs do not have. Both are paper investments; only one tracks gold directly.

What Does the Research Show?

Academic work on gold as a portfolio asset consistently shows low correlation with stocks over long horizons and meaningful diversification benefits at allocations of 5 to 10 percent. Studies comparing physical ownership against ETF exposure find nearly identical price tracking over multi-year horizons, with the ETF path delivering slightly higher net returns once fees are deducted (Source: Investopedia).

The limitation: most studies assume average fee levels and ignore the worst-case dealer markups that actually affect many Gold IRA buyers. Our own modeling suggests that when dealer markups reach 8% or more, the fee drag can take 2 to 3 years of metal appreciation to recover. Prevention is cheaper than recovery — verify the markup in writing before any physical metal purchase.

When should you talk to a specialist?

The choice between a Gold IRA and a gold ETF often benefits from a one-hour consultation with a fee-only CERTIFIED FINANCIAL PLANNER™, particularly when the allocation is meaningful.

- You are weighing an allocation above 15 percent. Concentration at that level changes the risk profile enough to warrant an independent second opinion.

- You are evaluating a sales pitch for a Gold IRA. A specialist can price-check dealer markups and identify numismatic overpricing before you commit.

- You have both taxable and retirement accounts to coordinate. Asset location planning — keeping gold in the IRA instead of a taxable account — requires modeling both at once.

- You are within 5 years of retirement. Liquidity planning becomes more expensive for physical metal closer to RMD age.

Frequently Asked Questions

What is the difference between a Gold IRA and a gold ETF?

A Gold IRA holds physical precious metals at an IRS-approved depository inside a retirement account. A Gold ETF is a paper security that tracks the price of gold and trades on a stock exchange like any other fund. The Gold IRA owns metal; the Gold ETF owns shares that represent claims on metal held by a trust.

Can I hold a gold ETF inside a Traditional IRA?

Yes. Gold ETFs like GLD, IAU, and SGOL can be held inside any standard brokerage IRA, including Traditional, Roth, and SEP IRAs. You get gold price exposure without the custodian, depository, or dealer markup costs of a Gold IRA. The account type determines tax treatment; the ETF determines the exposure.

Are gold ETFs taxed as collectibles?

Yes — when held in a taxable brokerage account. Gold ETFs are taxed at the 28% collectibles rate on long-term gains, not the 15% or 20% capital gains rate that applies to stocks. Inside an IRA, this collectibles rate does not apply — all withdrawals follow IRA distribution rules regardless of whether the asset is physical metal or an ETF.

Which is cheaper: Gold IRA or gold ETF?

Gold ETFs are significantly cheaper. Major gold ETFs charge expense ratios between 0.17% and 0.40% per year with no storage, custodian, or dealer markup fees. Gold IRAs typically cost $175 to $600 per year in fixed fees plus 3% to 10% dealer markup on every purchase. On a $100,000 account over 10 years, the difference can exceed $10,000.

The Bottom Line

The Physical vs Paper Question comes down to whether you actually need the metal in your hands. For most retirement investors, a gold ETF inside a Roth or Traditional IRA delivers the same price exposure at a fraction of the cost, with much better liquidity, and without the 28% collectibles tax that would apply in a taxable account. A Gold IRA wins only when physical ownership itself is the goal — and even then, the cost gap requires a long holding period and a large allocation to justify.

Before committing to either path, compare the all-in cost against your actual allocation size. Our Gold IRA fee breakdown shows the layers for the physical path, and our Gold IRA vs Traditional IRA overview covers the wrapper-level choice that sits upstream of this decision.

James Hartley

Former financial journalist (8 years) · Series 65 license holder

James covers retirement planning and precious metals investing. He spent eight years as a financial journalist before joining PrizeMining to research Gold IRA providers, fee structures, and regulatory requirements.

Sources

Gold IRA Due Diligence Checklist

10 items to verify before you open an account: fee transparency, custodian credentials, storage terms, buyback policies, and more. Free PDF, straight to your inbox.

No spam. Unsubscribe anytime. We never share your email.

This content is for informational purposes only and does not constitute financial, investment, or tax advice. Gold IRAs carry risks including price volatility, limited liquidity, and fees that can erode returns. Always consult a qualified financial advisor before making retirement investment decisions.