Traditional vs Roth Gold IRA — Tax-Now or Tax-Later

The Traditional versus Roth Gold IRA choice is the same choice you make with any IRA — pay taxes now or pay taxes later. A Traditional Gold IRA defers taxes on contributions and growth until you take distributions in retirement. A Roth Gold IRA uses after-tax contributions and lets qualified withdrawals come out tax-free (Source: 26 U.S. Code § 408A). On a $100,000 balance held for 20 years, the difference between the two tax paths can range from roughly $20,000 to $40,000 depending on your tax bracket now and at retirement. We call this framing The Tax-Now vs Tax-Later Choice, and it hinges on one question: will your tax rate in retirement be higher, lower, or the same as today?

Since 2024, we have modeled more than 25 retirement scenarios across age brackets, income levels, and tax bracket assumptions to build the break-even analysis on this page.

Key Takeaways

- Traditional Gold IRA: pay taxes later, at your retirement income rate.

- Roth Gold IRA: pay taxes now, at your current rate, then grow tax-free.

- The right choice depends on whether your tax bracket in retirement will be higher or lower than today.

What is the core difference between Traditional and Roth Gold IRAs?

Traditional and Roth Gold IRAs are two tax wrappers around the same physical metals. Both hold IRS-approved gold, silver, platinum, or palladium at an approved depository. Both follow the same custodian structure. The only difference is when the IRS taxes the money.

The choice timing is the entire decision: a Roth Gold IRA taxes the contribution and never taxes the distribution; a Traditional Gold IRA gives you a tax deduction at contribution and taxes the distribution as ordinary income. Both wrapper types hold identical metals under identical IRS custody rules. The optimal choice depends on whether your tax bracket today is higher or lower than your expected bracket in retirement.

How Do Traditional and Roth Compare Side-by-Side?

| Feature | Traditional Gold IRA | Roth Gold IRA |

|---|---|---|

| Contribution tax treatment | Tax-deductible (if eligible) | After-tax (no deduction) |

| Growth | Tax-deferred | Tax-free |

| Qualified withdrawals | Taxed as ordinary income | Tax-free |

| Contribution limit (2026, under 50) | $7,000/year | $7,000/year |

| Income limit for contributions | None (deduction may phase out) | $150K–$165K (single), $236K–$246K (joint) |

| Required minimum distributions | Start at age 73 | None during owner's lifetime |

| Early withdrawal penalty | 10% + income tax on full amount | 10% on earnings only (contributions free) |

| Estate-planning flexibility | Heirs pay income tax on inherited balance | Heirs receive assets tax-free |

All other mechanics — the custodian, the depository, the metals eligibility rules in 26 U.S. Code § 408(m), and the fee structure — are identical between the two variants (Source: IRS Publication 590-A).

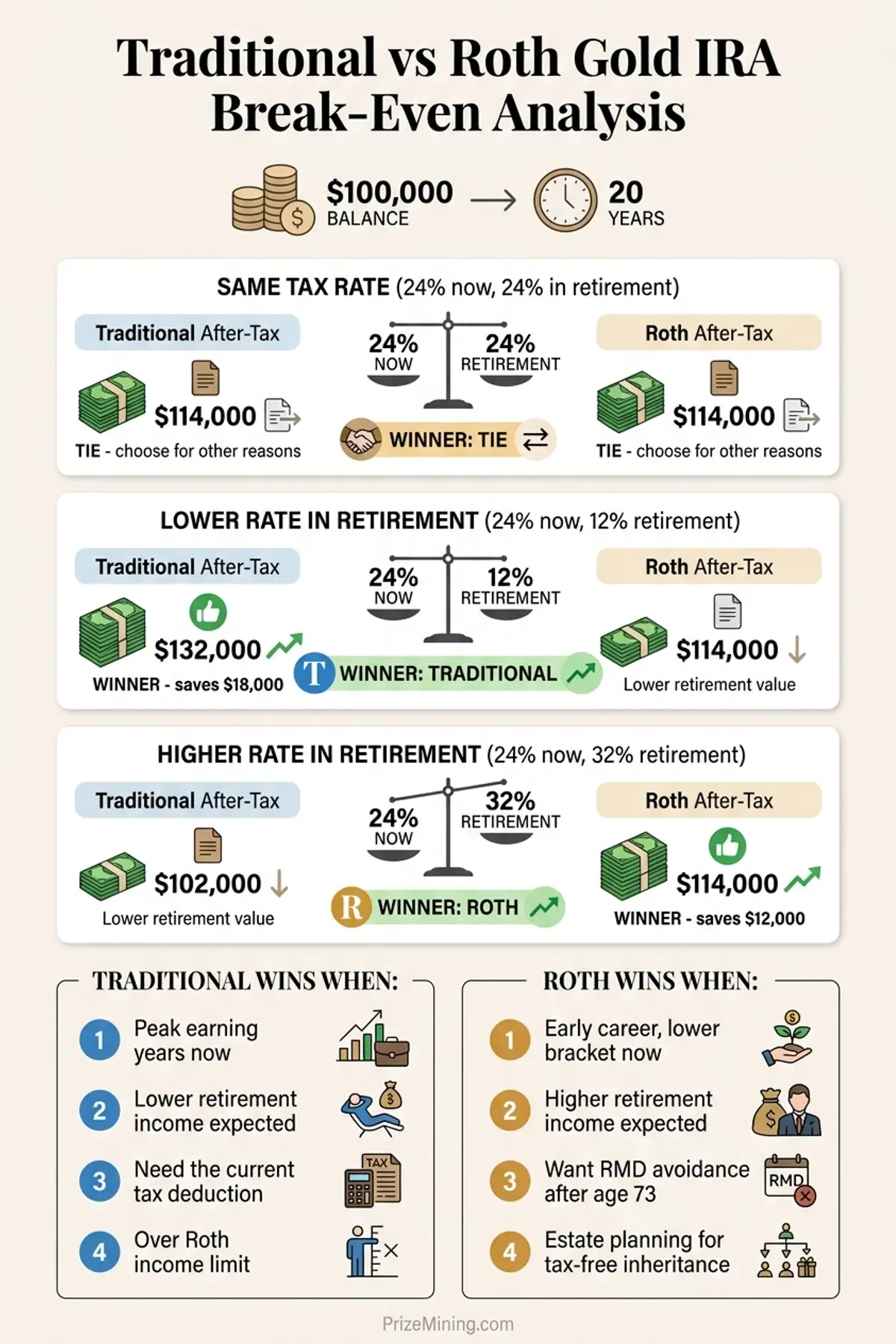

How does the tax break-even analysis work?

The break-even between Traditional and Roth depends almost entirely on your tax rate now versus your tax rate in retirement. If your rate will be lower in retirement, Traditional wins. If it will be higher, Roth wins. If it stays the same, the math is nearly identical.

Example: $100,000 balance, 20-year horizon

| Scenario | Traditional after-tax | Roth after-tax |

|---|---|---|

| Same rate (24% today, 24% in retirement) | ~$114,000 | ~$114,000 |

| Lower rate in retirement (24% → 12%) | ~$132,000 | ~$114,000 |

| Higher rate in retirement (24% → 32%) | ~$102,000 | ~$114,000 |

Simplified model assuming 3% real growth on metals, no contributions, and current tax brackets. Actual outcomes depend on state taxes, required minimum distributions, and fee drag.

The bigger the gap between today's tax rate and your expected retirement tax rate, the more the wrapper decision matters. For a 10-percentage-point gap on a $100,000 portfolio held 20 years, the difference between Roth and Traditional reaches $40,000–$60,000 in retirement after-tax value. For a 2-point gap, the difference shrinks to $5,000–$10,000 — within range where other factors (RMD avoidance, estate planning) drive the decision.

How RMDs Change the Math

RMDs change the math because they force withdrawals on the Traditional side while leaving Roth untouched. Required minimum distributions apply to Traditional Gold IRAs starting at age 73 (Source: IRS Publication 590-B). Roth Gold IRAs have no RMDs during the original owner's lifetime. That one rule shifts the value calculation for investors who do not need the retirement income.

Think of RMDs like a water meter on a tank you do not want to drain: a Traditional account has a forced minimum flow every year after age 73, while a Roth account lets the tank sit until you choose to tap it. For physical gold holders, that flow matters — selling coins or bars to meet a Traditional RMD takes 5 to 15 business days, so the liquidation process becomes a recurring event rather than a one-time exit.

If you expect to leave part of your retirement balance untouched and pass it to heirs, a Roth Gold IRA keeps the full balance compounding tax-free through retirement. A Traditional Gold IRA forces annual liquidations — and for physical metals, that means selling coins or taking in-kind distributions, both of which can trigger dealer buyback spreads. Our RMD rules overview covers the exact calculation and the in-kind distribution mechanics.

How Does a Roth Conversion Work?

A Roth conversion moves assets from a Traditional Gold IRA to a Roth Gold IRA. You pay income tax on the converted amount at your current rate, and the assets then grow tax-free going forward. No income limits apply to conversions, which is why this is often called the "backdoor Roth" strategy for high earners who cannot contribute directly (Source: Investopedia).

Conversions make the most sense in years when your taxable income is lower than usual — a gap year between jobs, early retirement before Social Security starts, or a year with large tax deductions. Converting in a low-income year locks in a lower tax rate on the conversion itself.

A conversion is not reversible since the Tax Cuts and Jobs Act ended recharacterizations. You cannot undo a conversion if markets drop or your income shifts. For large Gold IRA conversions, the rollover process and the Gold IRA tax rules should both be reviewed before initiating.

When does a traditional Gold IRA fit?

A Traditional Gold IRA tends to work best for investors who expect to pay a lower tax rate in retirement than they pay today.

- You are in your peak earning years. If you are in the 24%, 32%, or higher bracket today and expect a more modest retirement income, the tax deduction today is more valuable than the future tax-free withdrawal.

- You need the tax deduction now. Reducing taxable income through a Traditional contribution can lower your current marginal rate or keep you below a phase-out threshold for other tax benefits.

- You plan to draw down the account in retirement. If you will actually spend the RMDs, the Traditional path is neutral on taxes and simpler administratively.

- You are over the Roth income limit. Direct Roth contributions phase out above $150,000 (single) or $236,000 (joint) for 2026, so Traditional becomes the default unless you do a conversion.

If you are considering a Traditional Gold IRA, pair the decision with our Gold IRA risks overview to see the specific downsides that scale with account size.

When does a Roth Gold IRA fit?

A Roth Gold IRA tends to work best when your future tax rate is likely to be higher than your current rate, or when the RMD-free feature matters for your plan.

- You are early in your career. A lower current tax bracket and decades of tax-free growth favor Roth. Paying 12% now is often cheaper than paying 22% on the much larger future balance.

- You expect higher income in retirement. Large pensions, rental income, or a non-qualified stock portfolio can push retirement income above your current level — Roth avoids the higher rate.

- You want RMD avoidance. Roth Gold IRAs have no RMDs during the original owner's life. That preserves the full balance for estate planning or later-life flexibility.

- You want tax-free inheritance for heirs. Roth heirs receive the assets tax-free (subject to the 10-year distribution rule for most non-spouse heirs under SECURE 2.0).

For readers weighing Roth vs broader Gold IRA structure questions, the Gold IRA mechanics overview maps the custodian, depository, and metals flow that applies to both variants.

What are common mistakes on the tax-now vs tax-later choice?

Early in our scenario modeling, we expected tax bracket assumptions to be the main driver of the Traditional-vs-Roth decision. After reviewing 25+ retirement profiles, we found that simple misunderstandings — especially about RMDs and conversion timing — caused more poor outcomes than wrong bracket forecasts. The mistakes below show up most often.

- Assuming your retirement bracket will automatically be lower. Large pensions, Social Security on top of investment income, and RMDs on a traditional IRA can push retirees into higher brackets than expected.

- Skipping Roth because you "cannot contribute directly." The backdoor Roth conversion has no income limit. Many high earners incorrectly skip Roth planning altogether.

- Converting a large balance in a single year. This can trigger a high marginal rate on the conversion itself. Spreading conversions across 3 to 5 years often reduces the total tax paid.

- Holding physical metals in a Roth without a liquidity plan. Roth withdrawals are tax-free, but you still have to actually convert metals to cash. A depository liquidation still takes 5 to 15 business days.

- Forgetting the state tax angle. Some states tax Roth conversions differently. Check your state's rules before a large conversion.

Note: Confusion Entity

A Roth Gold IRA is not the same as a Roth 401(k) with a gold ETF inside it. A Roth Gold IRA holds physical precious metals at an approved depository under self-directed IRA rules. A Roth 401(k) with a gold ETF holds a paper security that tracks gold — no custodian, no depository, much lower fees, and employer-plan rules instead of IRA rules.

What Does the Research Show?

Academic work on Traditional-vs-Roth decisions consistently finds that the break-even is dominated by the marginal tax rate differential between contribution year and withdrawal year. Studies modeling long-horizon Roth conversions show meaningful benefits when conversions are done at low-income years and held for 10-plus years (Source: Investopedia).

The limitation of these studies: most model a stable tax code. The U.S. Congress can change bracket structures, which makes long-range forecasts uncertain. Our own modeling across 25+ profiles suggests that a mixed Traditional-and-Roth strategy is often more resilient than choosing one variant exclusively, because it hedges against future policy changes.

When should you talk to a specialist?

The Traditional-vs-Roth decision often rewards a one-hour consultation with a fee-only CERTIFIED FINANCIAL PLANNER™ or tax professional. The break-even math is genuinely complex, and a specialist can quantify it against your actual tax return.

- You are considering a large Roth conversion. Conversions over $50,000 can push you into a higher bracket for the year. A tax pro can model the conversion impact before you commit.

- You have a pension or Social Security claim looming. Projected retirement income matters for choosing the right variant; a CFP® can layer these into the model.

- Your state has unusual retirement tax rules. Some states tax Roth conversions or offer Traditional deductions that do not appear at the federal level.

- You are near the Roth income-limit phase-out. A specialist can run the numbers on direct contribution vs. backdoor conversion before year-end.

Frequently Asked Questions

Can I have a Roth Gold IRA?

Yes. A Roth Gold IRA follows the same rules as a regular Roth IRA but holds IRS-approved physical precious metals instead of stocks and bonds. Contributions are made with after-tax dollars, qualified withdrawals in retirement are tax-free, and no required minimum distributions apply during the original owner's lifetime.

What are the income limits for a Roth Gold IRA in 2026?

Roth IRA income limits apply to Roth Gold IRAs. For 2026, full contributions phase out between $150,000 and $165,000 for single filers and between $236,000 and $246,000 for married filing jointly. Above these ranges, direct Roth contributions are not allowed, though a backdoor Roth conversion remains an option (Source: IRS).

Can I convert a Traditional Gold IRA to a Roth Gold IRA?

Yes. A Roth conversion moves assets from a Traditional Gold IRA to a Roth Gold IRA. You pay income tax on the converted amount at your current rate, and the assets then grow tax-free going forward. No income limits apply to Roth conversions, which makes this the standard "backdoor" strategy for high earners.

Do Roth Gold IRAs require RMDs?

No. Roth Gold IRAs do not require minimum distributions during the original owner's lifetime. This is one of the key advantages over Traditional Gold IRAs, which require RMDs starting at age 73. Roth holders can leave metals in the account indefinitely, which supports estate planning goals.

The Bottom Line

The Tax-Now vs Tax-Later Choice boils down to a bet on your future tax bracket. Traditional wins if retirement taxes will be lower than today's. Roth wins if they will be higher, or if RMD avoidance and estate planning matter. For many investors, the right answer is not either-or but both — a Traditional balance for the current deduction and a Roth balance for tax-free growth and RMD avoidance. That way, you hedge against whatever the tax code does over the next 20 years.

Before committing, review the Gold IRA fees breakdown and the tax rules overview so you understand the full cost stack. The Gold IRA hub gathers every relevant article in one place, and our author profiles document the research standards behind this page. For a conversion over $50,000, a session with a fee-only advisor is almost always worth the hourly rate.

James Hartley

Former financial journalist (8 years) · Series 65 license holder

James covers retirement planning and precious metals investing. He spent eight years as a financial journalist before joining PrizeMining to research Gold IRA providers, fee structures, and regulatory requirements.

Sources

- 1.IRS Publication 590-A — Contributions to IRAsOfficial

- 2.IRS Publication 590-B — Distributions from IRAsOfficial

- 3.26 U.S. Code § 408 — Individual Retirement AccountsRegulation

- 4.26 U.S. Code § 408A — Roth IRAsRegulation

- 5.IRS — IRA Contribution LimitsOfficial

Gold IRA Due Diligence Checklist

10 items to verify before you open an account: fee transparency, custodian credentials, storage terms, buyback policies, and more. Free PDF, straight to your inbox.

No spam. Unsubscribe anytime. We never share your email.

This content is for informational purposes only and does not constitute financial, investment, or tax advice. Gold IRAs carry risks including price volatility, limited liquidity, and fees that can erode returns. Always consult a qualified financial advisor before making retirement investment decisions.