Gold IRA Rollover

A Gold IRA rollover moves retirement money into a precious metals account through one of three funding paths. The IRS allows three methods, each with different tax rules and deadlines. Choosing the wrong path can trigger thousands in unexpected taxes. Below you will learn all three options, the timeline, and the mistakes to avoid.

Key Takeaways

- Three funding paths exist: direct rollover, indirect rollover, and trustee-to-trustee transfer, each with different rules.

- Indirect rollovers carry the highest risk: a 60-day deadline, mandatory 20% withholding from employer plans, and a once-per-year limit.

- Talk to a fee-only advisor or your plan administrator before initiating a rollover to confirm eligibility and avoid costly missteps.

What Is a Gold IRA Rollover?

A Gold IRA rollover moves retirement funds from an existing account, such as a 401(k), 403(b), TSP, or traditional IRA, into a self-directed IRA that holds physical gold and other approved precious metals. The account itself operates under the same IRS rules as any traditional IRA, as outlined in IRS Publication 590-A. The difference is what it holds: bars and coins in an approved depository instead of stocks and bonds in a brokerage account.

Gold IRA advertising uses “rollover” for both rollovers and transfers, but the IRS treats them differently. The distinction affects three things: tax exposure (transfers have no withholding; indirect rollovers do), deadlines (transfers have no 60-day clock; indirect rollovers do), and frequency (one IRA-to-IRA indirect rollover per 12 months; transfers are unlimited).

To understand how the account itself is structured once funds arrive, see our overview of how a Gold IRA works.

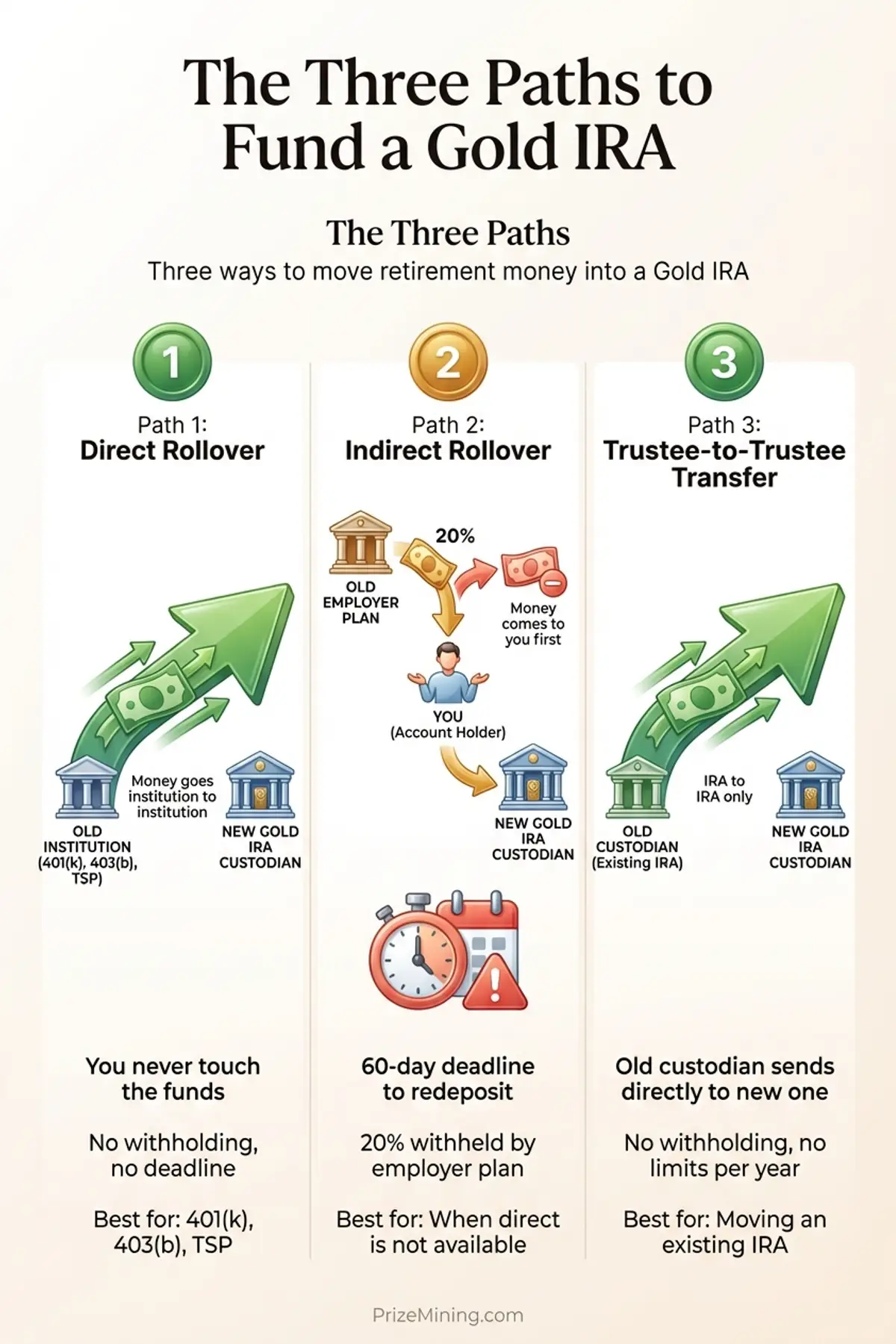

What Are the Three Paths to Fund a Gold IRA?

Three paths fund a Gold IRA: a direct rollover (trustee-to-trustee, no withholding), an indirect rollover (paid to you, 60-day deadline, withholding rules apply), or a trustee-to-trustee transfer (between IRAs of the same type, simplest and lowest risk). The table below summarizes how each handles withholding, deadlines, and frequency limits.

| Path | How It Works | Tax Risk | Timeline | Best For |

|---|---|---|---|---|

| Direct rollover | Old plan sends funds straight to new custodian | Low | 2 – 4 weeks | 401(k), 403(b), TSP to Gold IRA |

| Indirect rollover | Old plan sends funds to you; you forward them within 60 days | High | Depends on you | Situations where direct rollover is unavailable |

| Trustee-to-trustee transfer | Old IRA custodian sends funds directly to new IRA custodian | Lowest | 1 – 3 weeks | IRA to Gold IRA |

Early in our research, we assumed direct rollovers and transfers were interchangeable. After tracking the actual paperwork, we found that transfers bypass the plan administrator entirely, which eliminates the risk of withholding or missed deadlines. The distinction is practical, not just technical.

Path 1 — Direct Rollover

A direct rollover moves funds straight from your old plan to your new Gold IRA custodian without passing through your hands. You instruct the employer plan administrator to send the funds directly to the receiving custodian. The check is made payable to the new custodian “for the benefit of” you, or the funds move electronically. No withholding applies, and no 60-day clock starts (Source: IRS Rollovers of Retirement Plan and IRA Distributions).

Because you never take possession of the money, a direct rollover avoids the mandatory 20% federal income tax withholding that applies to indirect rollovers from employer plans. There is no 60-day deadline to worry about and no once-per-year limit. For most people moving funds from a 401(k), 403(b), or TSP into a Gold IRA, the direct rollover is the safest and most straightforward path.

The main drawback is speed. Some plan administrators take ten to fifteen business days to process a direct rollover request, and the timeline is largely outside your control. Ask your plan administrator for their estimated processing time before you start.

Path 2 — Indirect Rollover

An indirect rollover is like being handed an envelope of cash with a 60-day countdown. Your old plan sends the funds to you, and you then deposit them into your new Gold IRA within 60 calendar days. If you miss that deadline, the IRS treats the entire amount as a taxable distribution. If you are under 59½, you may also owe a 10% early withdrawal penalty on top of the income tax (Source: IRS Publication 590-A).

Indirect rollovers from employer-sponsored plans come with an additional complication: mandatory 20% withholding. Your old plan is required to withhold 20% of the distribution for federal taxes before sending you the check. You receive only 80% of your balance. To complete the rollover in full, you must deposit 100% of the original amount into the new IRA using your own cash to cover the withheld portion. If you deposit only what you received, the missing 20% becomes a taxable distribution.

The IRS also limits you to one indirect rollover per 12-month period across all of your IRAs. A second indirect rollover within that window is treated as a taxable distribution and may also be subject to a 6% excess contribution penalty if deposited into an IRA (Source: IRS Publication 590-A).

Given these risks, an indirect rollover generally only makes sense when a direct rollover is not available, for instance if your plan administrator does not support direct transfers to self-directed IRA custodians.

Path 3 — Trustee-to-Trustee Transfer

A trustee-to-trustee transfer moves funds directly between two IRA custodians. You fill out a transfer request form at the new custodian, and the two institutions handle the wire or check. You never receive the funds personally. No withholding applies, no 60-day clock starts, and the one-rollover-per-12-months rule does not apply to transfers.

Transfers are not reported as distributions on your tax return, carry no 60-day deadline, and have no once-per-year limit. You can transfer between IRAs as many times as you need. This makes transfers the lowest-risk method for moving money between IRA accounts (Source: IRS Publication 590-A).

The catch is that transfers only work between IRA accounts. If your money is in an employer plan like a 401(k), a transfer is not an option. You would need a direct rollover instead.

Which Accounts Can You Roll Over?

Eight retirement account types qualify for a rollover into a Gold IRA: traditional 401(k), 403(b), Thrift Savings Plan, traditional IRA, SEP IRA, SIMPLE IRA (after 2 years), Roth 401(k) (only to a Roth Gold IRA), and Roth IRA (only to a Roth Gold IRA). Each carries different timing and employer-restriction rules, listed in the table below (Source: IRS Rollovers of Retirement Plan and IRA Distributions).

| Account Type | Can Roll Over? | Restrictions |

|---|---|---|

| Traditional 401(k) | Yes | May require separation from employer or in-service distribution eligibility |

| 403(b) | Yes | Same separation or in-service rules as 401(k) |

| Thrift Savings Plan (TSP) | Yes | Must be separated from federal service or eligible for age-based withdrawal |

| Traditional IRA | Yes | Transfer preferred; no employer restrictions |

| SEP IRA | Yes | Transfer preferred; funds treated as traditional IRA assets |

| SIMPLE IRA | Yes, after 2 years | Must wait two years from first contribution or face a 25% penalty |

| Roth 401(k) | Yes, to a Roth IRA | Cannot roll into a traditional Gold IRA; must go to a Roth self-directed IRA |

| Roth IRA | Yes, to a Roth IRA | Transfer to a Roth self-directed IRA; cannot convert to traditional |

The single most common hurdle is the “current employer” restriction: most 401(k) plans block rollovers while you are still employed with the sponsoring company. Some plans permit in-service distributions at age 59½ or older — confirm this with your plan administrator before opening a Gold IRA account. Without that confirmation, you may complete the Gold IRA setup only to find your funds cannot be moved.

How Long Does a Rollover Take?

Most Gold IRA rollovers take two to four weeks from start to finish, though delays at the originating plan can stretch the timeline. Here is a typical breakdown of each step.

| Step | Duration | What Can Delay It |

|---|---|---|

| Open the self-directed IRA | 1 – 3 business days | Incomplete paperwork, identity verification issues |

| Request rollover from old plan | 1 – 5 business days | Plan administrator backlogs, missing forms |

| Funds arrive at new custodian | 5 – 15 business days | Check vs. wire processing, plan administrator processing times |

| Purchase metals | 1 – 3 business days | Dealer inventory, price confirmation delays |

| Ship metals to depository | 2 – 5 business days | Shipping logistics, depository intake processing |

The longest delay usually comes from the originating plan. Some large 401(k) administrators process direct rollovers in five business days. Others take two to three weeks, particularly if they require a notarized form or a medallion signature guarantee. Ask for the expected timeline before you submit your request so you can plan accordingly.

Be aware that fees begin accruing once your new self-directed IRA is open, even before the rollover funds arrive. Some custodians charge the setup fee at account opening, not at funding.

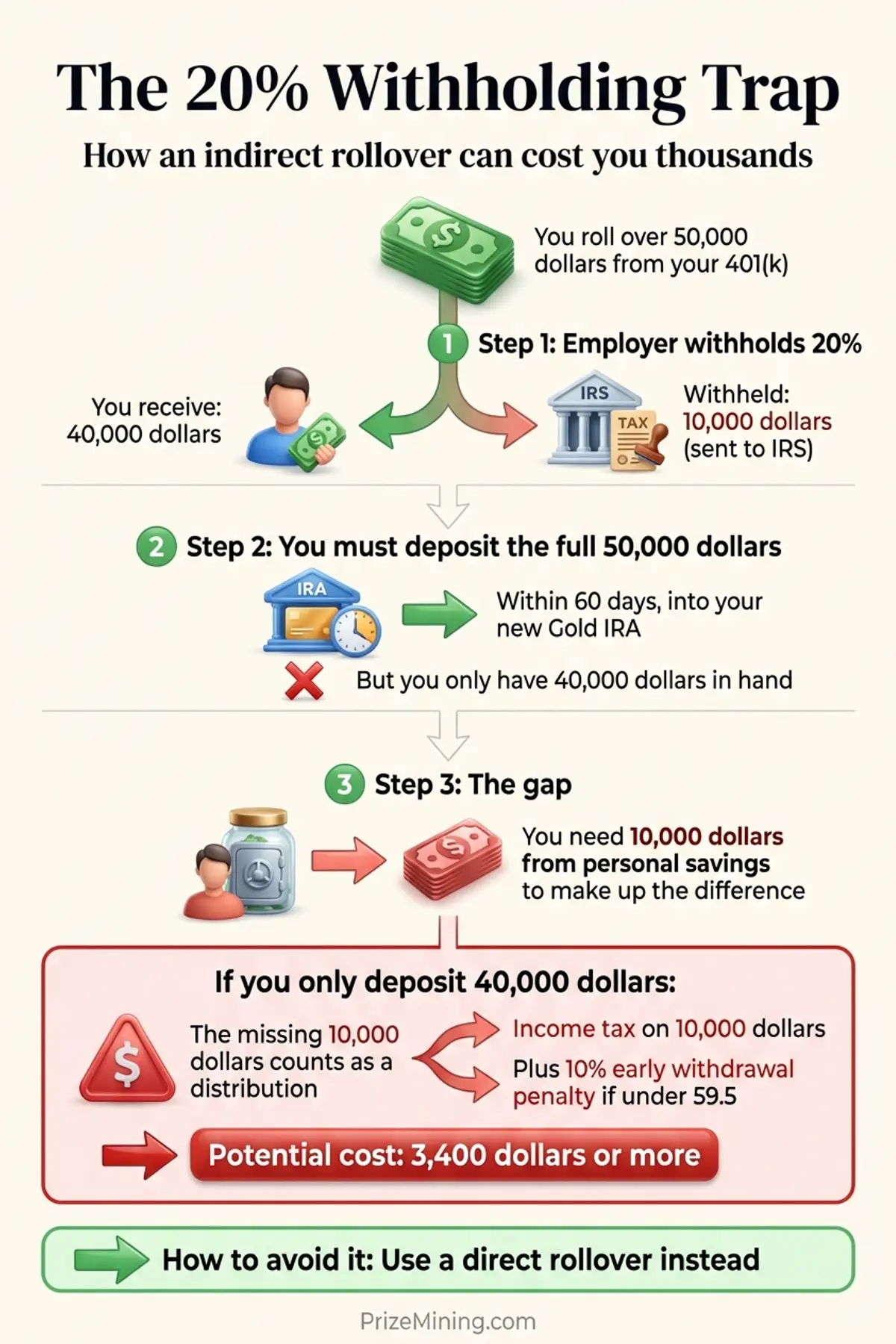

How Does the 20% Withholding Trap Work?

The indirect rollover withholding rule catches more investors than any other rollover mistake. Here is how the math works on a $50,000 balance, step by step.

You request a distribution of $50,000 from your 401(k). Your plan administrator is required by law to withhold 20% for federal income tax before sending the check. That means you receive $40,000, not $50,000. The withheld $10,000 goes to the IRS as a tax prepayment (Source: IRS Rollovers of Retirement Plan and IRA Distributions).

To complete the rollover without any tax consequences, you must deposit the full $50,000 into your Gold IRA within 60 days. Since you only received $40,000, you need to come up with $10,000 from other savings to make up the difference. If you deposit only the $40,000 you received, the IRS treats the missing $10,000 as a taxable distribution. Depending on your tax bracket, you could owe $2,200 to $3,700 in income tax on that amount, plus a $1,000 early withdrawal penalty if you are under 59½.

You can recover the $10,000 withholding when you file your tax return, assuming you completed the full rollover. But you still need the extra cash up front, and the recovery does not happen until tax filing season the following year.

This is why most financial professionals recommend the direct rollover path for employer plan distributions. With a direct rollover, no withholding applies because the funds never pass through your hands (Source: SEC Investor Alert on Self-Directed IRAs).

Before you start

Not sure if your account qualifies or which path to take? Use our rollover readiness checklist to confirm eligibility, identify your best funding path, and avoid common pitfalls before contacting a provider.

How does a rollover differ from a transfer?

A rollover moves funds from an employer-sponsored plan (401(k), 403(b), TSP) to an IRA and is reported on IRS Form 1099-R. A transfer moves funds from one IRA to another IRA, custodian to custodian, and is not reported as a distribution. Three concrete differences matter: 1099-R reporting (rollover yes, transfer no), once-per-year limit (rollover yes, transfer no), and withholding exposure (rollover yes if indirect, transfer no).

A rollover moves funds from an employer-sponsored plan (401(k), 403(b), TSP) to an IRA. In a direct rollover, the plan sends funds to the new custodian. In an indirect rollover, the plan sends funds to you, and you forward them. Both are reported on IRS Form 1099-R.

A transfer moves funds from one IRA to another IRA. The money goes directly from custodian to custodian. The IRS does not treat a transfer as a distribution, so it does not appear on a 1099-R and does not count toward the once-per-year indirect rollover limit (Source: IRS Publication 590-A).

In practice, the choice depends on where your money is today. If it is in an employer plan, you need a rollover. If it is already in an IRA, a transfer is simpler, faster, and carries less risk. If a Gold IRA provider tells you to “roll over” your existing IRA, ask whether they actually mean a trustee-to-trustee transfer. The paperwork, reporting, and rules are different.

For a broader look at how taxes affect Gold IRA accounts beyond the rollover step, see our Gold IRA tax rules overview.

What rollover mistakes do investors make most often?

Five rollover mistakes account for most expensive errors: missing the 60-day deadline on an indirect rollover, attempting a second indirect rollover within 12 months, depositing only the net amount after withholding, rolling over from a current employer plan without confirming eligibility, and confusing a rollover with a transfer. Each is detailed below with the financial consequence.

- Missing the 60-day deadline on an indirect rollover. The countdown starts the day you receive the distribution, not the day you requested it. Calendar days count, not business days. If day 60 falls on a weekend, the deadline is still day 60 unless you qualify for one of the narrow IRS hardship exceptions. Once the 60-day window expires, the full distribution becomes taxable income automatically. Setting a calendar reminder for day 45 gives you a buffer.

- Attempting a second indirect rollover within 12 months. The once-per-year rule applies across all of your IRAs, not per account. If you completed an indirect rollover from any IRA in the past 12 months, a second one results in a taxable distribution and may trigger a 6% excess contribution penalty (Source: IRS Publication 590-A).

- Depositing only the net amount after withholding. On a $50,000 indirect rollover from a 401(k), you receive $40,000 after the mandatory 20% withholding. Depositing only $40,000 means the IRS treats the missing $10,000 as a distribution. You must contribute the full $50,000 from your own funds to avoid the tax hit.

- Rolling over from a current employer plan without checking eligibility. Many 401(k) plans do not permit rollovers while you are actively employed. Starting the Gold IRA process before confirming eligibility wastes time and may result in custodian fees on an account you cannot fund.

- Confusing a rollover with a transfer. Requesting a “rollover” from your existing IRA when you mean a “transfer” can result in unnecessary tax reporting. Always specify “trustee-to-trustee transfer” when moving funds between IRA accounts.

Gold IRA providers process rollovers regularly and can guide you through the paperwork. However, they are not tax advisors. For questions about tax consequences specific to your situation, consult a tax professional or fee-only financial advisor before initiating any rollover.

When is a Gold IRA rollover not the right move?

A Gold IRA rollover is not the right move in five situations: your employer 401(k) match would be lost, your account is below $25,000 (fees consume too much), your time horizon is under 5 years, your tax bracket is dropping in retirement (Roth-favorable scenario), or your existing IRA already covers the metals exposure you want via an ETF. Each scenario below includes the calculation.

- Your current 401(k) has very low fees and good investment options. Some employer plans offer institutional-class index funds with expense ratios below 0.05%. Moving those funds into a Gold IRA, which carries custodian fees, storage fees, and dealer markups, may increase your overall costs substantially. Compare total annual costs side by side before deciding.

- You are close to a critical age where timing creates tax complications. If you are approaching 59½ or 73, the timing of a rollover can interact with early withdrawal penalties or required minimum distribution schedules in ways that increase your tax bill. A rollover initiated at the wrong moment can trigger an RMD shortfall or lock you out of penalty-free access to funds you need soon.

- You have outstanding 401(k) loans that would become immediately taxable. If you carry a loan balance against your 401(k) and roll over the remaining funds, the outstanding loan is typically treated as a distribution. That means income tax on the full loan amount, plus a 10% early withdrawal penalty if you are under 59½. Pay off the loan before initiating a rollover.

- Your total retirement balance is too small for Gold IRA fees to make sense. Gold IRA custodians charge flat annual fees for administration and storage, typically $200 to $500 per year. On a $25,000 account, that represents 0.8% to 2% of your balance annually, before dealer markups. Those costs can erode a small account faster than the metals appreciate.

When a Rollover May Be the Right Move

- You have a former-employer 401(k) sitting idle. Old plans often sit in default target-date funds with limited oversight. Rolling those funds into an IRA you control, whether a Gold IRA or a standard brokerage IRA, restores decision-making to you.

- Your current plan charges high administrative fees. Some 401(k) plans layer record-keeping fees on top of fund expenses. If your total plan cost exceeds 1% per year, a direct rollover to a low-cost IRA structure can reduce the fee drag measurably.

- You want to consolidate multiple retirement accounts. Combining three old 401(k) accounts plus two traditional IRAs into a single custodian simplifies record-keeping, RMD planning, and beneficiary designations as you near retirement.

- You have completed your tax analysis and a Gold IRA fits the plan. If a tax professional has confirmed that a precious metals allocation works within your retirement strategy, a direct rollover is the safest funding path to execute that decision.

When to Talk to a Financial Advisor

Consider consulting a fee-only financial advisor before proceeding if:

- You have outstanding 401(k) loans that might become taxable.

- You are between age 55 and 59½ and want to understand the Rule of 55 implications.

- You are considering rolling over more than $100,000 and want independent tax advice.

What Should You Do First?

Before you contact a Gold IRA provider, take three preliminary steps that can save you time, money, and paperwork headaches.

- Confirm your account is eligible. Call your plan administrator and ask whether your account permits rollovers, whether you need to be separated from your employer, and what forms are required. This five-minute call prevents weeks of wasted effort.

- Decide which path fits your situation. If your money is in an employer plan, a direct rollover is typically the safest route. If your money is already in an IRA, a trustee-to-trustee transfer is simpler and carries fewer restrictions. Avoid the indirect rollover unless no other option exists.

- Compare providers before committing. Rollover paperwork ties you to a specific custodian once submitted. Review our fee breakdown and compare provider fee structures, processing timelines, and customer reviews before you start.

Talk to a fee-only advisor or your plan administrator before initiating a rollover. An independent review of your situation can identify whether a Gold IRA fits within your broader retirement plan, or whether other options deserve consideration first.

Next step

Ready to see if your account qualifies? Start the rollover readiness checklist or return to the Gold IRA resource center for the complete overview.

Moving retirement funds into a Gold IRA involves real decisions with real tax consequences. The three paths, direct rollover, indirect rollover, and trustee-to-trustee transfer, serve different situations and carry different levels of risk. Picking the wrong path, missing a deadline, or depositing the wrong amount can turn a straightforward process into an expensive mistake.

The safest approach is to confirm your eligibility first, choose the lowest-risk path available to you, and get professional guidance before submitting any paperwork. Providers will walk you through the process, but understanding the rules yourself puts you in a stronger position to ask the right questions and catch errors before they become costly.

James Hartley

Former financial journalist (8 years) · Series 65 license holder

James covers retirement planning and precious metals investing. He spent eight years as a financial journalist before joining PrizeMining to research Gold IRA providers, fee structures, and regulatory requirements.

Sources

Gold IRA Due Diligence Checklist

10 items to verify before you open an account: fee transparency, custodian credentials, storage terms, buyback policies, and more. Free PDF, straight to your inbox.

No spam. Unsubscribe anytime. We never share your email.

This content is for informational purposes only and does not constitute financial, investment, or tax advice. Gold IRAs carry risks including price volatility, limited liquidity, and fees that can erode returns. Always consult a qualified financial advisor before making retirement investment decisions.