Gold IRA Liquidation

Gold IRA liquidation is harder than putting money in. Buyback spreads between the best and worst dealers can differ by over 4% on the same day (Source: SEC Investor Alert on Self-Directed IRAs). On a $100,000 liquidation, that gap is $4,000 you either keep or lose. This article covers both exit paths, the tax rules, and how to negotiate a better price.

In our review of more than 25 Gold IRA provider buyback policies, we documented the spread patterns, wire fees, and account closure charges summarized on this page. The figures reflect published schedules and confirmed quotes, not averaged marketing claims.

Key Takeaways

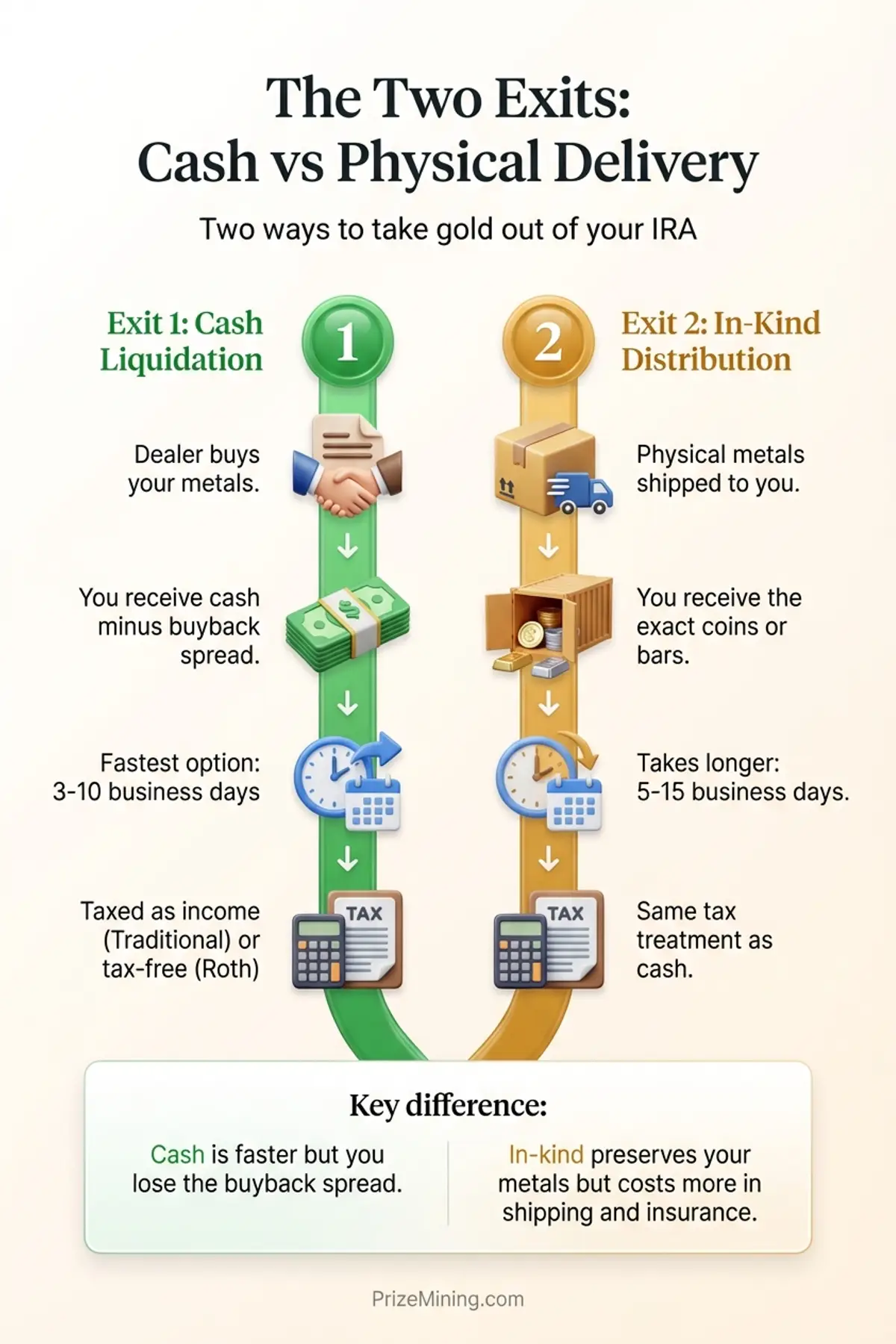

- Two ways out: sell metals for cash (cash liquidation) or receive the physical gold (in-kind distribution).

- Buyback prices run 1% to 5% below spot, so a $100,000 sale may net you only $95,000 to $99,000.

- Traditional IRA distributions are taxed as ordinary income; Roth distributions may be tax-free after age 59 and a half.

How do you get money out of a Gold IRA?

Two paths exit a Gold IRA: cash liquidation (sell metals to a dealer, receive dollars in the IRA account, then take a distribution) and in-kind distribution (custodian ships physical metals to you, treated as a taxable distribution at fair market value). Each path has different costs, timelines, and tax consequences. Cash liquidation typically takes 7–14 business days; in-kind distribution takes 14–30 business days due to insured shipping. Both trigger ordinary income tax on the distributed value.

For the broader account mechanics that lead up to liquidation, see our Gold IRA overview.

What are the two ways to exit a Gold IRA?

Cash liquidation is the more common exit: you sell metals to the dealer, receive dollars in the IRA, and then take a distribution. In-kind distribution skips the sale and ships the physical metals to you. Both trigger ordinary income tax on the distributed value because the IRS treats the fair market value of metals at distribution date as the taxable amount, as outlined in IRS Publication 590-B. The table below compares cost, timeline, and tax treatment.

| Factor | Cash Liquidation | In-Kind Distribution |

|---|---|---|

| What you receive | Dollars deposited into your IRA, then withdrawn | Physical gold or silver shipped to you |

| Buyback spread | Yes, 1% to 5% below spot | No spread, but shipping and insurance fees apply |

| Timeline | 3 to 10 business days | 2 to 4 weeks |

| Tax treatment | Taxed as ordinary income (Traditional) or potentially tax-free (Roth) | Same: fair market value counts as a distribution |

| Best for | Investors who need cash for expenses or want to reinvest | Investors who want to hold physical metals outside an IRA |

| Partial option | Yes, sell some metals and keep the rest | Yes, request delivery of specific items |

Most investors choose cash liquidation because they need the money for living expenses in retirement. In-kind distribution makes sense primarily for people who want to continue holding physical gold outside of the IRA structure, perhaps because they are closing the account but still believe in gold as a long-term asset. Either way, you should understand the full fee picture before initiating either exit.

How does the Gold IRA buyback process work?

The buyback process involves five sequential steps coordinated across three parties (custodian, depository, dealer): you submit a sell order to the custodian, the custodian instructs the depository to release the metal, the depository ships to the dealer or transfers internally, the dealer prices the metal at the buyback bid, and the proceeds settle in your IRA cash account. The full process takes 7–14 business days, longer if the depository requires physical shipment.

Step 1: Contact your dealer or custodian

You initiate the sale by contacting either your metals dealer or your custodian. Some custodians have a preferred buyback dealer; others allow you to shop around. Ask your custodian which dealers they work with and whether you are required to sell back to the original dealer. You are generally not obligated to, though some providers make it operationally easier to use their in-house buyback program (Source: Birch Gold).

Step 2: Get a buyback quote

The dealer will quote a price based on the current spot price minus their buyback spread. This quote is typically locked for a short window, often 24 to 72 hours. If you do not confirm within that window, the dealer requotes based on the current market price. Get the quote in writing.

Step 3: Custodian authorizes the sale

Because the metals are held in a tax-advantaged account, the custodian must authorize and process the transaction. You will typically sign a distribution or sale authorization form. The custodian then instructs the depository to release the metals to the dealer.

Step 4: Settlement and funding

Once the dealer receives and verifies the metals, they wire payment to your IRA account. Settlement typically takes 3 to 10 business days from the date you confirm the sale. After the cash lands in your IRA, you can request a distribution to your personal bank account, which may take an additional 1 to 3 business days. The entire process from initiation to cash in your bank can take one to three weeks.

How does buyback price differ from spot price?

This is where many investors feel blindsided. They watch the gold spot price, calculate what their holdings are worth, and then receive an offer that is noticeably less. The difference is the buyback spread, and it works against you just as the dealer markup worked against you when you bought.

When you purchased metals for your IRA, you paid a premium above spot price of 3% to 10%. When you sell them back, the dealer offers a price below spot of 1% to 5%. The two costs stack: round-trip cost is 4–15% of the position. On a $100,000 sale, the buyback spread alone costs $1,000–$5,000 (Source: US Money Reserve).

Here is what the math looks like on a $100,000 liquidation.

| Line Item | 1% Spread | 3% Spread | 5% Spread |

|---|---|---|---|

| Spot value of metals | $100,000 | $100,000 | $100,000 |

| Buyback spread deduction | –$1,000 | –$3,000 | –$5,000 |

| Wire transfer fee | –$25 | –$25 | –$25 |

| Account closure fee (if applicable) | –$150 | –$150 | –$150 |

| You receive | $98,825 | $96,825 | $94,825 |

| Total cost of selling | $1,175 | $3,175 | $5,175 |

The difference between the best-case and worst-case spread in this example is $4,000. That is money you keep or lose based entirely on which dealer you sell to and whether you negotiated the spread. And this table only shows the exit cost. When you add the original dealer markup from when you bought, the total round-trip cost can easily reach 8% to 15% of your investment.

How are Gold IRA liquidations taxed?

Liquidating a Gold IRA is a taxable event in most cases, and the rules depend on the type of IRA you hold and your age at the time of distribution. Getting this wrong can mean an unexpected bill from the IRS, so consult a qualified tax professional before you take a distribution. Our Gold IRA tax rules overview covers the broader tax picture in detail.

Traditional Gold IRA

Think of a Traditional Gold IRA distribution like a paycheck — the IRS treats every dollar as earned income and taxes it at your regular rate. Distributions from a Traditional Gold IRA are taxed as ordinary income at your current federal and state tax rate, as outlined in IRS distribution rules. If you liquidate $100,000, that amount is added to your taxable income for the year. Depending on your bracket, you could owe $12,000 to $37,000 in federal taxes alone. If you are under 59 and a half, an additional 10% early withdrawal penalty applies, adding $10,000 to that bill.

Roth Gold IRA

Qualified distributions from a Roth Gold IRA are potentially tax-free. To qualify, the account must have been open for at least five years and you must be 59 and a half or older. If both conditions are met, you pay no federal income tax on the distribution. If either condition is not met, the earnings portion of the distribution may be taxed and penalized.

Required minimum distributions

Traditional Gold IRA holders must begin taking required minimum distributions (RMDs) starting at age 73, as of current IRS rules. RMDs apply to the entire account, including metals. If you do not have enough cash in the account to cover your RMD, you may need to sell metals to generate the required amount. Failing to take an RMD triggers a 25% excise tax on the amount that should have been distributed (Source: IRS RMD FAQ). Roth IRAs do not require distributions during the original owner's lifetime.

In-kind distributions and taxes

If you take physical delivery of your metals instead of selling for cash, the IRS still treats it as a distribution. The fair market value of the metals on the date of distribution counts as taxable income for a Traditional IRA. You owe the same taxes whether you receive dollars or gold bars. Many investors do not realize this until after they have requested delivery.

How can you get the best price when selling?

Most articles about Gold IRA liquidation stop at explaining the process. They do not tell you how to negotiate a better outcome. Here are concrete steps that can put more money in your pocket when you sell.

1. Get quotes from at least three dealers

You are not always required to sell back to the dealer who sold you the metals. Ask your custodian whether they allow buybacks from other dealers. Then request written quotes from at least three dealers on the same day for the same products. The spread difference between dealers ranges 2 to 4 percentage points — that translates to $2,000–$4,000 on a $100,000 position. Our provider comparison worksheet can help you track quotes side by side.

2. Sell when gold is trending up, not during a panic

Dealers widen their buyback spreads during periods of high volatility or sudden price drops. When the market is calm and prices are stable or rising, spreads narrow by 1–2 percentage points. If your liquidation is not urgent, waiting for a calmer market environment improves your net price. Trying to time the gold market precisely is difficult, and the risks of holding too long should also factor into your decision.

3. Ask for the spread as a percentage, not just a dollar figure

Some dealers quote a dollar amount below spot, which can obscure the actual percentage. A dealer saying “we buy at $20 below spot per ounce” sounds modest, but if spot is $2,000, that is only 1%. If spot is $1,000, that same $20 is 2%. Always convert to a percentage and compare across providers.

4. Negotiate on larger liquidations

Dealers have more room to narrow the spread on larger transactions. If you are selling $50,000 or more in metals, ask whether they can improve the buyback price. A 0.5% improvement on a $100,000 sale is $500. The worst they can say is no.

5. Consider partial liquidation instead of selling everything at once

If you do not need all the money immediately, selling in stages lets you average your exit price across different market conditions. This approach also helps manage your tax liability by spreading distributions across multiple tax years, potentially keeping you in a lower bracket each year.

When is liquidating not the right move?

Liquidation is sometimes the right call, but not always. Before you initiate a sale, make sure none of these situations apply to you.

- Gold prices are significantly below your purchase price. Selling while the market is down locks in losses that you cannot undo. If your need for cash is not urgent, waiting for a recovery may preserve more of your original investment. That said, no one can predict when or whether prices will return to your cost basis.

- You have not compared buyback offers from multiple dealers. Accepting the first offer you receive is one of the most common and most expensive mistakes in Gold IRA liquidation. Spreads vary by 2 to 4 percentage points between dealers on the same day, and a single phone call to a second dealer can put thousands of dollars back in your pocket.

- You need the money within days. Cash liquidation typically takes 3 to 10 business days, and full account closure can stretch to several weeks. If you face an immediate expense, a Gold IRA is not a source of fast cash. Plan your liquidity needs well in advance.

- Your RMD amount is small enough to satisfy from other IRA assets first. If you hold multiple retirement accounts, you can satisfy your required minimum distribution from any combination of Traditional IRAs. Selling gold to cover a small RMD when you have cash in another IRA means absorbing the buyback spread unnecessarily.

When Liquidation May Be the Right Choice

- You have reached your required minimum distribution age. Once RMDs begin at 73, selling metals to meet the required amount is part of the normal account wind-down, and planned liquidation beats a forced sale later.

- You are rebalancing your overall retirement portfolio. If your precious metals allocation has drifted above your target percentage, a partial liquidation restores the mix without emptying the account.

- You face an emergency need and other liquid reserves are exhausted. A Gold IRA is not the fastest cash source, but if you have already drawn down other accounts, a planned liquidation with multiple buyback quotes can still produce acceptable results.

- A Gold IRA no longer fits your retirement plan. Circumstances change. If an updated financial plan, a new tax situation, or a change in retirement goals moves precious metals out of your strategy, an orderly exit through The Two Exits is better than leaving the account drifting.

When to Talk to a Financial Advisor

Consider consulting a fee-only financial advisor before proceeding if:

- You are unsure whether to take a cash or in-kind distribution.

- You want help timing a liquidation around RMDs or market conditions.

- You need guidance on the tax consequences of a large distribution.

What should you plan before you need to sell?

The best time to think about liquidation is before you open the account, not when you need the money. Like packing a parachute before you board the plane, planning your exit strategy while you still have time gives you more options and better outcomes.

- Ask about buyback terms before you buy. Every provider should be able to tell you their typical buyback spread and process. If they cannot or will not answer, that is a signal worth noting. Our Gold IRA overview lists the questions you should ask before committing.

- Understand your custodian's closure process. Some custodians charge account termination fees ranging from $50 to $250. Others require 30 days' written notice. Know these details before you need to act quickly.

- Keep records of what you paid. Documenting your original purchase prices, dealer markups, and fees helps you calculate your true cost basis. While the IRA tax treatment is based on distribution value rather than capital gains, this information is valuable if you take an in-kind distribution and later sell the metals outside the IRA.

- Plan for RMDs well in advance. If you are approaching 73, ensure your account has enough liquidity to meet required minimum distributions without being forced into an unfavorable buyback at the worst possible time.

- Talk to a tax professional. The interaction between Gold IRA distributions, Social Security income, and other retirement accounts can affect your overall tax bracket. A qualified advisor can help you sequence distributions to minimize your total tax burden over multiple years. This is especially important given the specific tax rules that apply to precious metals IRAs.

Liquidation is not an afterthought. It is the reason you opened the account in the first place: to eventually use those funds. The Two Exits, cash liquidation and physical delivery, each serve different goals, but both require forethought. Planning your exit with the same care you used to plan your entry means more of your money ends up where it belongs, in your hands.

James Hartley

Former financial journalist (8 years) · Series 65 license holder

James covers retirement planning and precious metals investing. He spent eight years as a financial journalist before joining PrizeMining to research Gold IRA providers, fee structures, and regulatory requirements.

Sources

Gold IRA Due Diligence Checklist

10 items to verify before you open an account: fee transparency, custodian credentials, storage terms, buyback policies, and more. Free PDF, straight to your inbox.

No spam. Unsubscribe anytime. We never share your email.

This content is for informational purposes only and does not constitute financial, investment, or tax advice. Gold IRAs carry risks including price volatility, limited liquidity, and fees that can erode returns. Always consult a qualified financial advisor before making retirement investment decisions.