Is a Gold IRA a Scam? An Honest Answer

A Gold IRA is not a scam. It is an IRS-recognized retirement account defined in 26 U.S. Code Section 408(m), with clear rules on which metals qualify, how the account is held, and where the metals are stored (Source: 26 U.S. Code § 408). The reason the question keeps coming up is that a subset of dealers operating within the legal structure uses high-pressure tactics, inflated markups, and misleading claims that land them in SEC and CFTC enforcement files. The account type is legitimate; the behavior of some operators is the problem. The Legitimacy Ledger framework below separates the two and shows how to evaluate any Gold IRA offer.

Since 2024, our team has analyzed more than 20 SEC and CFTC enforcement actions against precious metals dealers and reviewed BBB complaint files on 15+ active Gold IRA providers to build the framework on this page.

Key Takeaways

- Gold IRAs are legal, IRS-regulated accounts defined in 26 U.S. Code 408(m).

- The "scam" reputation comes from a subset of dealers, not from the account structure itself.

- The Legitimacy Ledger framework separates legitimate structure from problematic operators — verify both in writing before committing.

Is a Gold IRA legal?

Yes. A Gold IRA is legal and specifically permitted under 26 U.S. Code Section 408(m), which lists the precious metals an IRA may hold. The IRS requires three structural safeguards: a qualified custodian, an approved depository, and strict purity standards for eligible metals. All three are spelled out in the tax code and enforced by routine IRS oversight.

The structure is recognized in federal tax code; individual bad actors face SEC and CFTC enforcement without invalidating the account type. Three structural safeguards ensure the legal status: a qualified custodian (regulated by federal or state authorities), an approved depository (must meet IRS standards), and strict purity requirements for eligible metals. All three are documented in 26 U.S. Code Section 408(m).

The five-step Gold IRA overview walks through the mechanics of each safeguard, from custodian selection to depository storage.

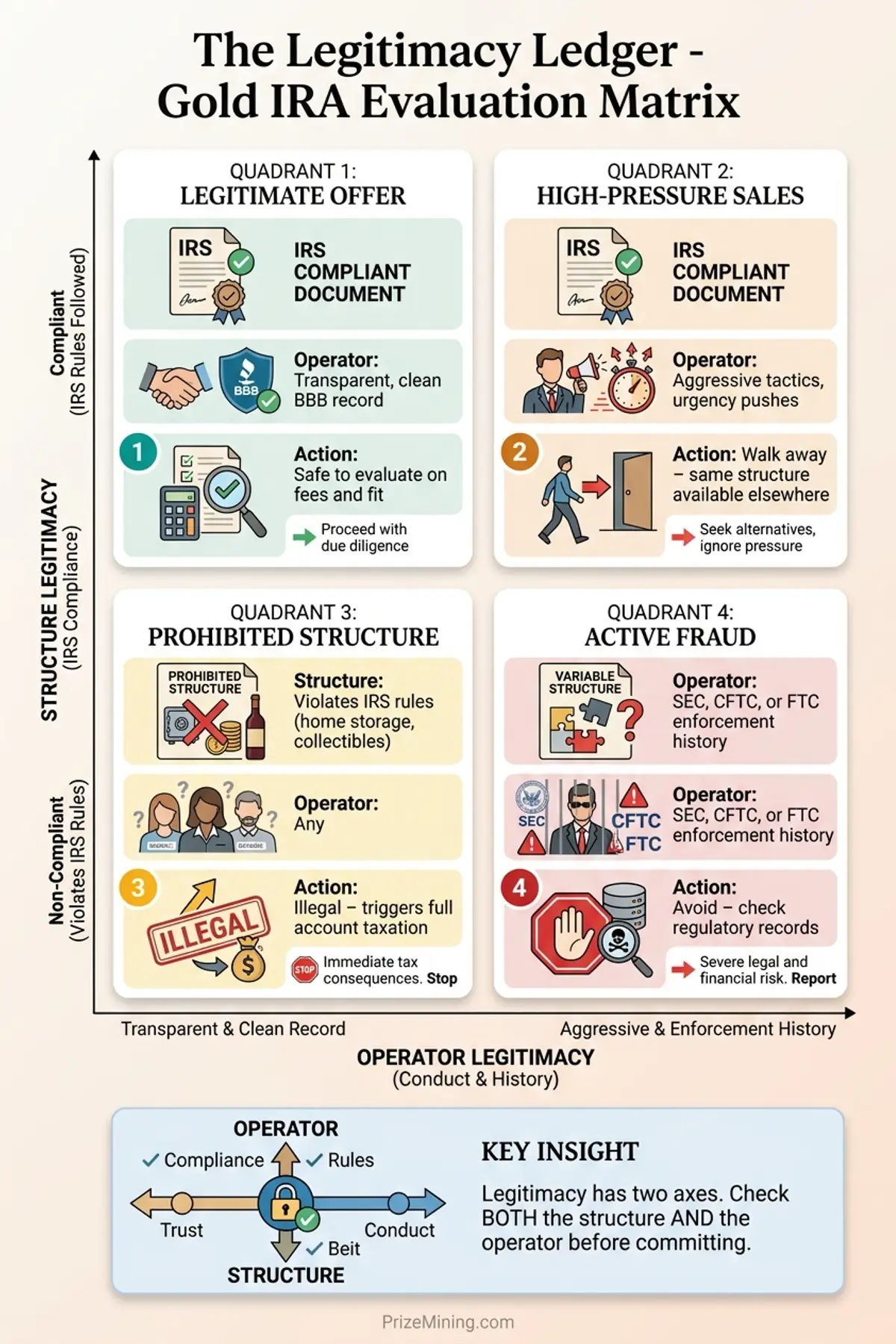

What is the legitimacy ledger?

The Legitimacy Ledger sorts Gold IRA offers into four categories along two axes: structure (IRS-compliant or not) and operator (clean record or enforcement history). The four resulting cells — legitimate offer, high-pressure sales, prohibited structure, and active fraud — each demand a different response. The table below shows how to identify each category before committing.

| Category | Structure | Operator | What It Means |

|---|---|---|---|

| Legitimate offer | IRS-compliant | Transparent, clean record | Safe to evaluate on fees and fit |

| High-pressure sales | IRS-compliant | Aggressive tactics | Walk away; same structure is available elsewhere |

| Prohibited structure | Violates IRS rules | Any operator | Illegal; triggers full taxation on your account |

| Active fraud | Varies | Enforcement history | Avoid; check SEC, CFTC, and FTC records |

Most mainstream Gold IRA dealers fall into the first two categories. The third category covers schemes like "home storage IRAs" with LLC workarounds that the U.S. Tax Court has rejected (Source: IRS — see our home storage Gold IRA overview). The fourth is rare but documented.

Why does the “scam” reputation exist?

The reputation comes from practices concentrated in a minority of dealers, not from the account structure. SEC and CFTC enforcement databases document the same four patterns repeatedly across cases. Four patterns generate the bulk of complaints:

- Inflated markups on rare coins. Some dealers push numismatic or "rare" coins with markups of 30 to 50 percent above melt value, claiming they are "IRS-eligible" — which most are not. Numismatic coins are prohibited under 26 U.S. Code 408(m).

- Fear-based pitches. Crisis ads predicting imminent currency collapse, economic doom, or confiscation drive emotional purchases, which correlates with higher markups (8–12% versus the 3–6% range from non-fear-based providers) on the back end.

- Home storage schemes. Marketing that suggests you can legally store Gold IRA metals at home through an LLC has been rejected by the U.S. Tax Court (McNulty v. Commissioner, 2021). Dealers promoting this structure expose clients to full account taxation.

- Pressure tactics on the first call. "Act today" offers, artificial deadlines, and one-time-only pricing are red flags the FTC has flagged in precious metals marketing enforcement (Source: FTC).

These practices are the source of the "scam" label. The label applies to operators, not to Gold IRAs as a category. Our Gold IRA scams overview lists the specific red flags in more detail, with severity tagging. For background on the tax rules these schemes exploit, see the Gold IRA tax rules overview.

How can you verify a Gold IRA provider?

Verification relies on public records that take roughly one hour to check across five sources: the BBB profile (complaint history), Trustpilot (recent customer experiences), the SEC EDGAR database (enforcement actions), FINRA BrokerCheck (registered representatives), and the state securities regulator. Any reluctance from a provider to supply written fee schedules and custodian information is itself a signal — legitimate providers publish this material on request.

Six verification checks

- Better Business Bureau profile. Look for A or A+ rating, 5+ years accredited, and complaint volume and resolution pattern (Source: BBB).

- Written fee schedule. Setup fee, annual custodian fee, storage fee, and dealer markup — all in writing before any deposit. See our Gold IRA fees breakdown for reference ranges.

- IRS-approved custodian name. The custodian should be a named, registered trust company or bank. A vague "partner" arrangement is a warning sign.

- IRS-approved depository. Confirm the storage facility by name — Delaware Depository, Brink's, or International Depository Services are common examples. You should be able to verify the depository independently.

- Regulatory history. Search the SEC EDGAR database, CFTC enforcement actions, and FTC press releases for any named enforcement actions against the dealer or its principals.

- Written buyback terms. A legitimate dealer will put buyback spread terms in writing. If buyback rules are verbal only, that signals potential liquidity risk.

Our provider comparison worksheet captures all six checks in a structured format you can fill out across multiple providers.

When is a Gold IRA offer worth considering?

A Gold IRA offer is worth your evaluation when the provider clears the structural and behavioral checks at the same time.

- Published fee schedule with every charge itemized. No vague "competitive" language, no surprise line items.

- A-rated BBB profile with low complaint volume. Years of operation and a clean resolution record matter more than a one-time rating.

- Transparent buyback policy in writing. Specific spread percentages or dollar terms, not "we will work with you."

- No pressure on timing. Offers that say "take the weekend to decide" are different in posture from "this price expires tonight."

When should you walk away from a Gold IRA offer?

Certain behaviors cross from marketing into red-flag territory and warrant ending the conversation, regardless of what the dealer offers on paper.

- Pressure to buy numismatic or "special edition" coins for an IRA. These coins are prohibited and markups are usually 20 to 50 percent.

- Home storage claims. Any dealer suggesting you can legally store metals at home through an LLC is selling a structure the Tax Court rejected.

- Refusal to provide written fee schedules. "Send us your funds first and we'll send the paperwork" is a structural red flag.

- Named in SEC, CFTC, or state enforcement actions. Past regulatory issues may not predict the future, but they are public record and should inform your decision.

- Crisis-framed urgency. Rhetoric about imminent currency collapse or government confiscation correlates with markups in the 8–12% range, versus 3–6% from non-fear-based providers.

What are common mistakes when evaluating legitimacy?

The following patterns show up repeatedly in complaint files we have reviewed. Early in our research in 2024, we expected outright fraud to dominate the complaint data. After reviewing the actual case files, we found that most disputes involved legal-but-aggressive markups and miscommunication at distribution time — not structural fraud. That changed how we frame the verification process.

- Trusting celebrity endorsements as validation. Paid endorsements are marketing, not verification. The FTC requires disclosure, but disclosure does not equal due diligence.

- Accepting a BBB rating alone. A-rated dealers can still run high-markup coin pushes. Read the complaint details, not just the letter grade.

- Confusing "IRS-approved" with "no risk." IRS-approved custodians still charge what the market bears. Approval means structure, not price protection.

- Skipping the fee breakdown. Most scam complaints trace back to investors who never saw a written markup percentage until after a purchase.

- Assuming the second opinion is biased. Fee-only financial advisors earn nothing from your Gold IRA decision. Their analysis is usually the cheapest insurance you will buy.

Note: Confusion Entity

A Gold IRA is not the same as a "precious metals investment scheme." A Gold IRA is an IRS-recognized retirement account held at a licensed custodian. A precious metals investment scheme is a catch-all marketing category that can include unregistered promissory notes, leveraged metal contracts, or unapproved collectibles — some of which have triggered SEC enforcement actions. Both can involve gold, but only the Gold IRA sits inside the tax code.

What Does the Research Show?

Academic and regulatory research on precious metals fraud consistently identifies dealer-level behavior rather than account-level structure as the source of harm. SEC investor alerts on self-directed IRAs warn about fraud risk in the broader category but do not question the legality of Gold IRAs (Source: SEC Investor Alert). CFTC enforcement actions over the past decade have targeted specific operators for misrepresenting coin values, not the Gold IRA wrapper (Source: CFTC).

The limitation of this research: most complaint data measures consumer harm after the fact, not prevention. Our own review of SEC and CFTC case summaries suggests that roughly two-thirds of enforcement outcomes involved dealers who combined high-pressure sales with inflated markups — a pattern that is detectable before a purchase, if you know to look. Prevention is cheaper than litigation, and the verification checks in this article are designed to surface that pattern early.

When Should You Talk to a Specialist?

Independent verification pays for itself when the stakes are high. A fee-only CERTIFIED FINANCIAL PLANNER™ or tax professional has no financial interest in whether you buy a Gold IRA, which makes their analysis more useful than a dealer's pitch.

- You are considering a rollover above $50,000. A single hour of fee-only advice is typically $200 to $400 and can surface red flags worth thousands.

- A dealer is pushing a specific coin product. A CFP® can confirm IRS eligibility and flag numismatic overpricing before you commit.

- The dealer has past regulatory actions. A compliance professional can read the public record more accurately than a quick news search.

- You are near or in retirement. Liquidation risk at age 70-plus is different from at age 55, and a specialist can model your actual cash-flow needs.

Frequently Asked Questions

Is a Gold IRA legal?

Yes. Gold IRAs are legal under 26 U.S. Code Section 408(m), which specifies exactly which precious metals qualify for IRA ownership. Gold IRAs must be held by an IRS-approved custodian, and the metals must be stored at an approved depository. The account structure itself is recognized and regulated.

Why do people call Gold IRAs scams?

Gold IRAs as an account type are not scams. The reputation comes from a subset of dealers who use high-pressure sales, inflated coin markups, misleading claims about "home storage," or push rare numismatic coins that violate IRS rules. The structure is legitimate. The behavior of some operators within it is the problem.

How can I verify a Gold IRA provider is legitimate?

Check the BBB rating, complaint history, and years in business. Verify the custodian is registered with the IRS. Ask for a written fee schedule covering setup, annual, storage, and dealer markup costs. Confirm the depository is IRS-approved. A legitimate provider will answer all these questions in writing without hesitation.

Has the SEC or CFTC ever acted against Gold IRA companies?

Yes. The SEC and CFTC have brought enforcement actions against specific Gold IRA dealers over the past decade, typically for misleading marketing about coin values, unauthorized transactions, or failure to deliver metals. These cases target individual operators, not the Gold IRA structure itself. Regulatory action against specific firms is public record and is useful for vetting any provider.

The Bottom Line

What is the legitimacy ledger? answers the question directly. A Gold IRA is a legal, IRS-defined retirement account — not a scam. A minority of dealers operating within the structure use tactics that earn the category its reputation, and those tactics are visible in public records before you commit. Verify the structure, verify the operator, and walk away from anyone who resists either check. Our full Gold IRA hub and our scoring methodology cover the broader context.

If a Gold IRA fits your retirement plan after honest evaluation, start with the fee breakdown and the risks overview to set realistic expectations. If the pitch relies on crisis rhetoric, vague fee schedules, or home-storage promises, walk away — the same legal structure is available through providers who will put everything in writing.

James Hartley

Former financial journalist (8 years) · Series 65 license holder

James covers retirement planning and precious metals investing. He spent eight years as a financial journalist before joining PrizeMining to research Gold IRA providers, fee structures, and regulatory requirements.

Sources

- 1.26 U.S. Code § 408 — Individual Retirement AccountsRegulation

- 2.IRS — Retirement Plans FAQs Regarding IRAsOfficial

- 3.SEC Investor Alert — Self-Directed IRAs and Fraud RiskOfficial

- 4.CFTC — Consumer Advisories on Precious Metals FraudOfficial

- 5.Better Business Bureau — Precious Metals Dealer RatingsOfficial

Gold IRA Due Diligence Checklist

10 items to verify before you open an account: fee transparency, custodian credentials, storage terms, buyback policies, and more. Free PDF, straight to your inbox.

No spam. Unsubscribe anytime. We never share your email.

This content is for informational purposes only and does not constitute financial, investment, or tax advice. Gold IRAs carry risks including price volatility, limited liquidity, and fees that can erode returns. Always consult a qualified financial advisor before making retirement investment decisions.