Gold IRA Fees Explained

Gold IRA fees consume 3% to 13% of your account in year one alone. Five charges stack: a one-time setup fee, an annual maintenance charge, a storage bill, a dealer markup on the metals, and a spread when you sell. Each fee looks small in isolation. Together they reduce a $100,000 retirement balance by $3,000 to $13,000 in the first year — and continue compounding annually thereafter.

Since 2024, our team has analyzed fee structures from more than 15 Gold IRA providers, comparing setup costs, annual charges, storage fees, and dealer markups across the industry. The numbers below reflect what we found, not what providers advertise on their landing pages (Source: SEC Investor Alert on Self-Directed IRAs).

Key Takeaways

- Gold IRA costs come from five stacked layers: setup, annual, storage, dealer markup, and buyback spread.

- First-year expenses on a $50,000 account typically range from $1,800 to $5,300, mostly from the dealer markup.

- Fixed fees hit smaller accounts harder, taking a larger percentage of your balance each year.

How Much Does a Gold IRA Cost?

A Gold IRA typically costs between $250 and $750 per year in custodian and storage fees alone. On top of those recurring charges, you pay a one-time setup fee and a dealer markup every time you buy metals. The total first-year cost on a $50,000 account can range from roughly $1,800 to $5,300, depending on the provider and the metals you choose.

Provider sales pages show one fee at a time. The setup fee looks reasonable in isolation. The annual fee looks manageable. The storage charge looks fair. What sales pages rarely show is the combined total — and they exclude the dealer markup from headline pricing. The full picture is the Fee Stack: five layers, applied by three different parties (custodian, depository, dealer).

What are the five layers of Gold IRA fees?

Five distinct fees apply to every Gold IRA account: a setup fee, an annual maintenance fee, a storage and insurance fee, a dealer markup on each metal purchase, and a buyback spread on each sale. Three parties collect them — the custodian, the depository, and the dealer — and each fee hits the account at a different point in the lifecycle.

| Fee Type | Typical Range | Who Charges It | When You Pay It |

|---|---|---|---|

| Setup fee | $50 – $200 | Custodian | Once, at account opening |

| Annual maintenance | $75 – $300 | Custodian | Yearly |

| Storage and insurance | $100 – $300/yr | Depository | Yearly (or quarterly) |

| Dealer markup | 3% – 10% above spot | Dealer | Each time you buy metals |

| Buyback spread | 1% – 5% below spot | Dealer | Each time you sell metals |

Three different parties collect these fees: the custodian (administrative), the depository (storage), and the dealer (metals supply). Investors who confuse the roles assume the custodian sets all prices and miss the largest cost in the stack — the dealer markup. Understanding who charges what enables you to negotiate or shop each layer separately. The five layers below explain each charge in order, starting with the setup fee.

Layer 1 — Setup Fees

The setup fee covers the administrative cost of opening your self-directed IRA account. Most custodians charge between $50 and $200 as a one-time charge. Some providers waive the setup fee entirely, especially on accounts above $50,000. A waived setup fee is not automatically a good deal, since the savings may reappear as a higher dealer markup elsewhere in the Fee Stack.

Layer 2 — Annual Maintenance Fees

Annual maintenance fees (also called custodian or administration fees) cover IRS reporting, account statements, and ongoing record-keeping. The typical range is $75 to $300 per year. Two pricing structures exist: flat-dollar (regardless of balance) and percentage-based (typically 0.25% to 0.50% of account value). The flat-fee model costs less above $50,000; the percentage model costs less below $50,000 (Source: IRS Publication 590-A).

Layer 3 — Storage and Insurance Fees

IRS rules require your metals to be held at an approved depository, not at home. Depositories charge for vault space and insurance coverage. Expect to pay $100 to $300 per year, depending on the value stored and the type of storage you choose.

Segregated storage, where your exact coins and bars are kept separate from other investors' holdings, costs more than commingled storage, where your metals are pooled with others. Segregated storage typically runs $150 to $300 per year, while commingled storage may cost $100 to $150. Segregated storage guarantees you receive the same items you purchased when you take a distribution. Commingled storage returns equivalent items, not necessarily yours.

Layer 4 — Dealer Markups and Premiums

A dealer markup is like the retail price at a car dealership: the sticker price sits above wholesale, and the spread varies by dealer. When you buy gold for your IRA, the dealer sells it at a premium above the current spot price. Markups typically range from 3% to 10%, though some dealers push higher on certain products (Source: Yahoo Finance).

On a $50,000 metals purchase, a 5% markup means you pay $2,500 more than the spot value of the gold. A 10% markup doubles that to $5,000. The markup is the single largest cost in most Gold IRA transactions, yet it is also the least transparent. Many providers quote markups only over the phone and do not publish them on their websites.

When we first built our fee comparison in 2024, we focused on the numbers providers publish on their websites. After requesting complete fee schedules by phone, we found that published fees often excluded wire transfer charges, account termination fees, and the actual dealer markup on metals. The markup differences between providers were far larger than the differences in custodian fees.

Layer 5 — Buyback Spreads

Buyback spreads sit 1% to 5% below the current spot price when you sell. Combined with the 3–10% markup you paid at purchase, the round-trip cost of entering and exiting a position reaches 4–15% of the metal's spot value. On a $100,000 position held 10 years, the round-trip cost alone consumes $4,000–$15,000 before any of the annual fees apply (Source: World Gold Council market structure data).

Some providers advertise a “guaranteed buyback” program. The guarantee means they will buy back your metals, not that they will pay spot price. Always ask what the typical buyback spread is before you open an account.

What Does a Gold IRA Cost Per Year?

The table below shows estimated first-year and ongoing annual costs for two common account sizes. These figures use mid-range estimates from our provider research and assume a single metals purchase at account opening.

| Fee | $50,000 Account | $100,000 Account |

|---|---|---|

| Setup fee (one-time) | $100 | $100 |

| Annual maintenance | $175 | $175 |

| Storage and insurance | $200 | $200 |

| Dealer markup (5%) | $2,500 | $5,000 |

| Wire transfer | $30 | $30 |

| First-year total | $3,005 | $5,505 |

| Annual cost (year 2+) | $375 | $375 |

The first year is the most expensive because of the dealer markup and setup fee. After year one, ongoing costs drop to $375 per year in custodian and storage fees for both account sizes, assuming you do not purchase additional metals. Every additional purchase adds another markup layer.

These are mid-range estimates. Your actual costs could be lower with a competitive provider or higher with a premium-priced one. You can estimate your specific costs with our Gold IRA fee estimator tool.

Estimate your costs

Want numbers specific to your situation? Use our fee estimator to calculate first-year and long-term costs based on your account size and provider.

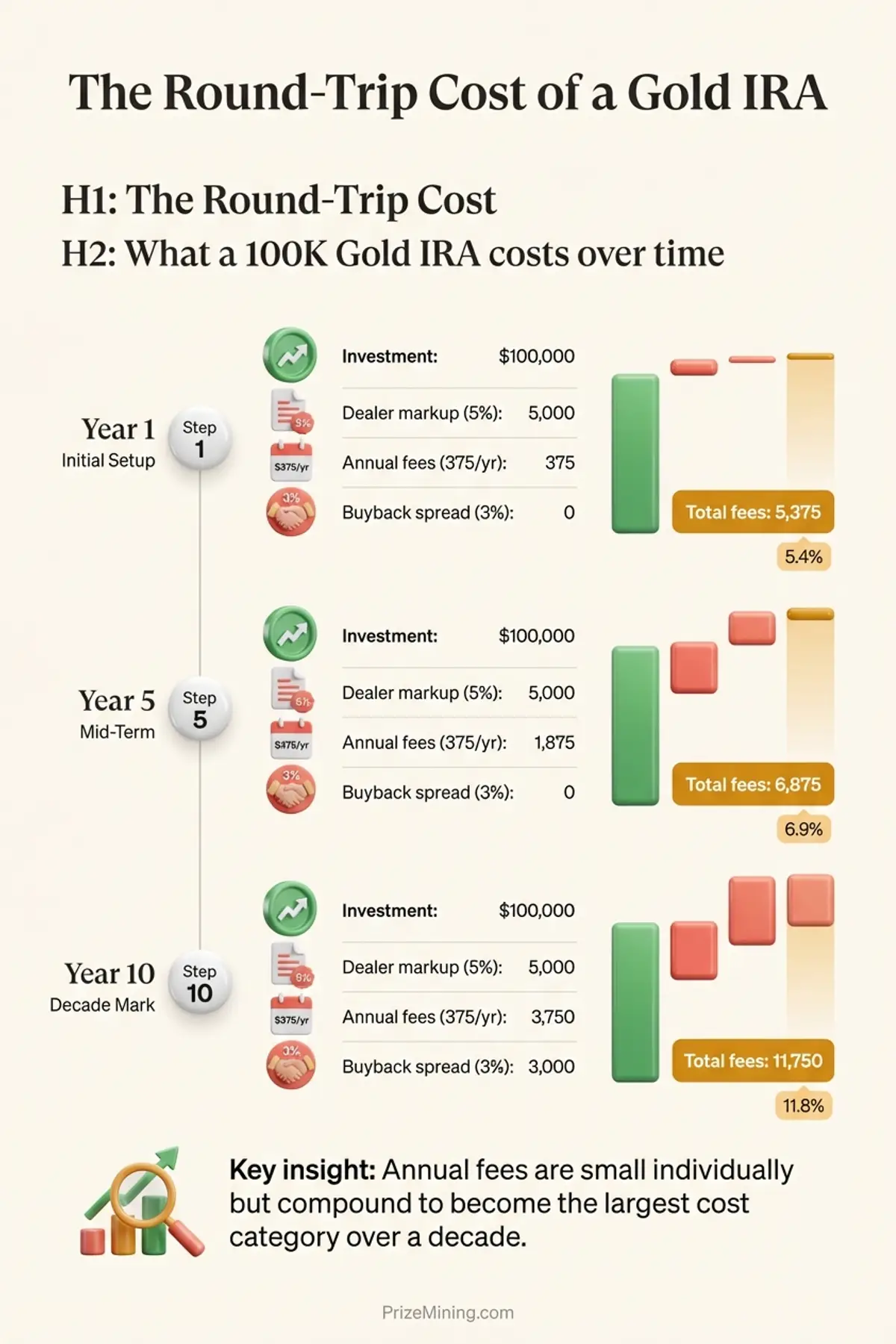

What does a Gold IRA cost over 5 and 10 years?

A $100,000 Gold IRA can cost roughly $11,750 in total fees over ten years once you add the markup going in, annual fees while holding, and the buyback spread coming out. Most fee comparisons only show year one. The round-trip cost captures the full cycle.

The table below uses mid-range estimates: a 5% dealer markup, $375 per year in custodian and storage fees, and a 3% buyback spread at liquidation (Source: SEC Investor Alert on Self-Directed IRAs).

| Cost Category | Year 1 | Year 5 | Year 10 |

|---|---|---|---|

| Setup fee | $100 | $100 | $100 |

| Dealer markup (5%) | $5,000 | $5,000 | $5,000 |

| Custodian + storage fees | $375 | $1,875 | $3,750 |

| Wire transfers | $30 | $30 | $30 |

| Buyback spread (3%) | $3,000 | $3,000 | $3,000 |

| Round-trip total | $8,505 | $10,005 | $11,880 |

| As % of $100K | 8.5% | 10.0% | 11.9% |

If you invest $100,000 in a Gold IRA and sell everything after five years, the total fees may consume roughly $10,000, or 10% of your original investment. After ten years, the total climbs to nearly $11,900. Gold would need to appreciate by at least that much just to break even on fees before you see any real return.

For a $50,000 account, the round-trip costs are lower in absolute dollars but higher as a percentage of your balance. The fixed custodian and storage fees represent a larger share of a smaller account, which is why minimum account sizes matter. Fees are one of several factors that can erode long-term returns, and our Gold IRA risks overview covers other factors worth weighing before you commit.

Which Fee Model Costs Less?

The flat-fee model costs less for accounts above $50,000; the percentage model costs less for accounts below $50,000. The breakeven point sits exactly there in the example below: $250 flat versus 0.50% of balance. Knowing your account size determines which model maximizes your retained returns.

| Account Size | Flat Model (~$250/yr) | % Model (0.50%/yr) | Which Saves More |

|---|---|---|---|

| $25,000 | $250 | $125 | Percentage model |

| $50,000 | $250 | $250 | About equal |

| $100,000 | $250 | $500 | Flat fee model |

| $250,000 | $250 | $1,250 | Flat fee model |

| $500,000 | $250 | $2,500 | Flat fee model |

The breakeven point in the example above sits near $50,000. Below that amount, a percentage-based model costs less. Above it, the flat fee wins, and the advantage grows as your balance increases. On a $500,000 account, the difference is $2,250 per year, or $22,500 over ten years.

Fixed fees also create a disproportionate drag on smaller accounts. The table below shows how the same $375 in annual fixed fees (custodian plus storage) consumes a different share depending on account size.

| Account Size | Fixed Annual Fees | As % of Account | Impact on Returns |

|---|---|---|---|

| $25,000 | $375 | 1.50% | High drag, gold must rise 1.5%/yr just to cover fees |

| $50,000 | $375 | 0.75% | Moderate drag, comparable to a managed fund |

| $100,000 | $375 | 0.38% | Low drag, fees are a small share of returns |

| $500,000 | $375 | 0.08% | Minimal drag, fixed fees are nearly negligible |

For accounts under $25,000, the annual fee drag alone may make a precious metals IRA difficult to justify on a cost basis. At $100,000 and above, fixed fees become a much smaller percentage and the cost structure begins to look more reasonable relative to other investment vehicles (Source: Investopedia).

When does a “free” Gold IRA setup cost more?

A “free” Gold IRA setup typically costs $2,300 more than a paid one over the first transaction. The waived setup fee shifts to the dealer markup: a provider offering free storage charges 8–10% over spot, while a provider with a standard $100 setup fee charges 3–5%. On a $50,000 purchase, the difference is $2,500 — far more than the $150 in waived storage costs.

The most common shift lands on the dealer markup. A provider offering free storage for the first year may charge an 8% to 10% markup on metals, compared to 3% to 5% at a provider with standard storage fees. On a $50,000 purchase, the difference between a 5% and a 10% markup is $2,500. A year of waived storage fees typically saves $150 to $200. The “free” promotion costs $2,300 more than paying the storage fee directly.

Some providers also offset fee waivers through wider buyback spreads. A company that waives the setup fee may offer 4% to 5% below spot on buybacks, while a company that charges a $100 setup fee may offer 1% to 2% below spot. On a $100,000 liquidation, that 3-percentage-point difference is $3,000, thirty times the $100 setup fee you “saved.”

The pattern also extends to “free coins” or “bonus silver” promotions. The cost of those promotional metals is baked into the markup on the metals you actually order. Ask the provider for a line-by-line breakdown of the price per ounce versus the current spot price. If the premium is above 5%, the promotion may be costing you more than it appears.

How do Gold IRA fees differ from dealer markups?

Custodian fees cover account administration; dealer markups are the profit margin on each metal purchase. Custodians are regulated financial institutions; dealers are separate companies. Custodian fees are published in advance; dealer markups are negotiated per transaction. Mixing the two prevents accurate provider comparison.

Custodian fees cover account administration: opening the account, annual record-keeping, IRS reporting, and processing transactions. The custodian is a financial institution regulated by state or federal agencies. Custodian fees are usually published on the provider's website or available in a fee schedule (see 26 U.S. Code § 408).

Dealer markups are the profit margin the metals dealer earns on every sale. The dealer is a separate company from the custodian, though some Gold IRA companies bundle both roles or have preferred dealer relationships. Markups vary by product, by dealer, and by market conditions. They are rarely published and often require a phone call to confirm.

When a provider quotes “fees of $250 per year,” that figure typically covers only the custodian and storage fees — not the dealer markup. The dealer markup is the largest single cost in your account at 3–10% of each purchase, and it routinely sits outside the quoted “fee” number. Always ask: “Does your fee quote include the dealer premium on metals?” A no answer means you are seeing only part of the Fee Stack.

Our review methodology page explains how we evaluate fee transparency for every provider we review, including whether they disclose markups before you commit.

When is a Gold IRA not worth the fees?

A Gold IRA is not worth the fees in four specific situations: account balance below $25,000 (fixed fees consume 1–1.5% per year), time horizon under 5 years (8–15% round-trip cost requires similar appreciation just to break even), reliance on regular investment income (gold pays no dividends), and direct comparison against a total-market index fund (0.03–0.20% expense ratio versus 0.50–1.50% for a Gold IRA). Each situation below explains the math.

- Your account is below $25,000. Fixed annual fees of $250 to $375 consume 1% to 1.5% of a small account every year. A low-cost index fund IRA charges a fraction of that. The math improves only once your balance is large enough to absorb the fixed costs without dragging down returns (Source: Investopedia).

- Your time horizon is under five years. The round-trip cost of entering and exiting, including dealer markup and buyback spread, can reach 8% to 15%. Gold needs to appreciate by that amount just for you to break even. Short holding periods rarely allow enough appreciation to overcome the fee drag.

- You need regular income from your investments. Gold does not pay dividends or interest. Your return comes entirely from price appreciation. If your retirement plan depends on periodic income, dividend stocks, bonds, or REITs may serve you better at a lower fee level.

- You are comparing against a total-market index fund. A broad market index fund in a traditional IRA typically costs 0.03% to 0.20% per year with no markups, no storage fees, and no buyback spreads. The fee gap between a Gold IRA and an index fund IRA is substantial. You can read more about these trade-offs in our Gold IRA risks article.

Ask a fee-only financial advisor to model the fee impact on your specific account size and time horizon before committing. An hour of independent advice can clarify whether the costs make sense for your situation.

When Gold IRA Fees May Make Sense

- You hold $100,000 or more in retirement assets. At that balance, the $250 to $500 in fixed annual fees represents 0.25% to 0.50% per year, which is in line with managed mutual funds.

- You plan a 5% to 10% allocation to precious metals. A modest allocation spreads the fee drag across a smaller share of your portfolio, and the diversification benefit can justify the extra cost layer.

- Your time horizon is 10 years or longer. Long holding periods give appreciation more time to absorb the one-time dealer markup, which is the largest single Fee Stack cost.

- You have a clear diversification mandate from your financial plan. If an advisor recommended physical metals as part of an overall strategy, the structural costs of a Gold IRA become the price of executing that plan correctly.

What are the most common Gold IRA fee mistakes?

Investors who overpay for a Gold IRA typically make one of four errors early in the process: comparing only the custodian fee (ignoring 4 of 5 layers), ignoring the buyback spread (which can exceed several years of annual fees), falling for “free” promotions (which shift cost to the dealer markup), or skipping written quotes (verbal estimates are unenforceable). Each error and its cost is detailed below.

- Comparing only the custodian fee. The custodian fee is one layer of the Fee Stack. Investors who choose the cheapest custodian sometimes pay more overall because the associated dealer charges higher markups or the depository charges above-average storage fees. Compare the total cost across all five layers.

- Ignoring the buyback spread. The spread you lose when selling metals can exceed several years of annual fees combined. Ask for the buyback spread in writing before purchasing. A provider that quotes a 5% buyback discount costs you $5,000 on a $100,000 liquidation.

- Falling for “free” promotions. Setup fee waivers, free first-year storage, or bonus metals almost always correspond to higher dealer markups elsewhere. Calculate the total first-year cost, not just the line items labeled as fees.

- Not getting written quotes. Verbal fee estimates are unenforceable. Request a complete written fee schedule that lists every charge, including wire fees, termination fees, and the specific markup on the products you plan to purchase (Source: FTC Disclosure Guidelines).

How can you reduce Gold IRA fees?

Five practical steps reduce Gold IRA fees by 30–60% versus accepting the first quote: compare at least three providers before committing, negotiate the dealer markup (the largest single layer), choose a flat-fee custodian above $50,000, request a buyback-spread commitment in writing, and consolidate purchases to minimize repeated markups. Gold IRA fees are not fixed by regulation (Source: IRS Publication 590-B) — every layer is negotiable or shoppable.

1. Compare at least three providers before committing

Request a complete written fee schedule from each provider, including setup fees, annual fees, storage fees, and the markup on two or three specific products. Side-by-side comparison often reveals that the lowest-advertised provider is not the cheapest once all five layers are added up. You can use our provider comparison worksheet to track each provider's fees side by side.

2. Choose bullion bars over premium coins when possible

Dealer markups on bars run 1–3 percentage points lower than markups on coins. A 1-ounce gold bar carries a 3% to 4% premium; a 1-ounce American Gold Eagle carries 5% to 7%. Both qualify for an IRA. The bar saves $1,000–$3,000 at purchase on a $100,000 buy and has a tighter buyback spread when you sell.

3. Consolidate purchases to reduce per-transaction fees

Some custodians charge a wire transfer fee ($25 to $50) and a transaction fee for each purchase. Making one larger purchase instead of several smaller ones can reduce these recurring charges. If you plan to add metals over time, batch your purchases quarterly or annually rather than monthly.

4. Negotiate on larger accounts

Providers often have room to reduce fees on accounts above $100,000. Custodians may waive setup fees, dealers may lower markups, and some offer reduced storage rates for high-value holdings. Ask directly. The worst outcome is they say no.

5. Ask a fee-only financial advisor to review the fee schedule

A fee-only advisor charges a flat rate or hourly fee and does not earn commissions on product sales. They have no financial incentive to steer you toward a particular provider. Paying $200 to $300 for an hour of independent advice can save thousands over the life of your account by identifying hidden costs and recommending lower-cost alternatives. If you are considering a rollover from a 401(k) or existing IRA, an advisor can also help you weigh the fee impact of moving those funds.

What Should You Ask Before Opening an Account?

Five specific questions can reveal whether a provider is transparent about costs or hiding fees behind vague language. Before you open an account, ask each provider the following and compare their answers in writing (Source: IRS Publication 590-A).

- What is your complete fee schedule? Ask for setup fee, annual maintenance fee, storage fee, wire transfer fee, and account termination fee, all in a single document. If they cannot provide one, consider that a warning sign.

- What is the markup on specific products? Ask for the premium above spot price on a 1-ounce gold bar and a 1-ounce American Gold Eagle. Compare these across providers. A provider who refuses to quote specific markups before you commit may charge more than average.

- What is your typical buyback spread? Ask how much below spot they offer when purchasing metals back from clients. Get the number in writing.

- Are there termination fees? Some providers charge $100 to $250 to close your account or transfer metals to a different custodian. Know the exit cost before you enter.

- What is the total first-year cost on my account size? Ask them to calculate the combined total of all fees and markups for your planned investment. A reputable provider should be willing to put this number in writing.

Deceptive fee practices remain a concern in the Gold IRA industry. Our Gold IRA scams article covers the most common tactics and how to protect yourself. For a broader understanding of how precious metals retirement accounts work, the Gold IRA resource center connects all of our articles, tools, and provider reviews (Source: FTC Disclosure Guidelines).

Next step

Ready to compare costs across providers? Use our provider comparison worksheet to track fees side by side, or read the Gold IRA risks overview to understand the other factors that affect your long-term returns.

Gold IRA expenses come in five stacked layers, and every layer matters. The Fee Stack, from the one-time setup charge at the bottom to the buyback spread at the top, determines how much of your investment actually works for you. Providers who publish one fee while hiding four others make it difficult to compare on an equal basis.

The best defense is a complete, written fee schedule that shows every layer of The Fee Stack from every provider you consider. Compare the full cost, not just the headline number. And remember: fees are a certainty, while returns are not. Understanding exactly what you will pay, across every level of The Fee Stack, is the first step toward making a well-informed decision about whether a Gold IRA fits your retirement plan.

James Hartley

Former financial journalist (8 years) · Series 65 license holder

James covers retirement planning and precious metals investing. He spent eight years as a financial journalist before joining PrizeMining to research Gold IRA providers, fee structures, and regulatory requirements.

Sources

Gold IRA Due Diligence Checklist

10 items to verify before you open an account: fee transparency, custodian credentials, storage terms, buyback policies, and more. Free PDF, straight to your inbox.

No spam. Unsubscribe anytime. We never share your email.

This content is for informational purposes only and does not constitute financial, investment, or tax advice. Gold IRAs carry risks including price volatility, limited liquidity, and fees that can erode returns. Always consult a qualified financial advisor before making retirement investment decisions.